Internal Rate of Return, or IRR, is a financial metric used to analyze the profitability of potential investments. When analyzing investments it is common to utilize IRR in conjunction with net present value, or NPV.

IRR formulas utilize similar calculations as NPV calculations, but the two yield different outputs. On the one hand IRR is a percentage that represents a rate of return, discount rate, or interest rate while NPV is a dollar value that represents the present value of future cash inflows and outflows.

What Is IRR?

IRR is a metric that represents an estimated discount rate that would return a net present value of zero when performing a discounted cash flow (DCF) analysis.

Simply put, it is the rate of return required for an investment’s present value of cost to equal its present value of future cash flows.

In discounted cash flow analysis, the discount rate is the rate used to calculate the present value of future cash flows and represents the time value of money.

When viewed from the lens of net present value, the discount rate represents either the cost of capital to make an investment or the expected rate of return on an investment. Therefore, IRR is a discount rate and represents the rate required to drive the net present value of future cash flows to zero.

This might seem counterintuitive as a net present value of zero is considered neutral. However, when NPV, is zero it means that the investment earns a rate of return equal to the discount rate.

This makes understanding IRR much easier because an investment that uses a 10% discount rate that returns an NPV of zero indicates the investment would yield a 10% return.

The term Internal Rate of Return refers to the calculation excluding external factors. In many financial calculations risk-free rates, inflation, tax rate, and other inputs are required. IRR calculations exclude these factors and focus only on internal cash flows and “terminal” value.

IRR calculations can be performed backward-looking to determine the actual returns of an investment and forward looking to estimate future returns.

The biggest benefit of using IRR is that it can give the owner of any business—from a small business to a large corporation—the ability to see immediately which projects have the highest potential cash flow.

Why Is IRR Important?

IRR calculations are important and helpful for a few reasons.

First, the calculation considers time as a component and therefore is very helpful for analyzing future cash flows.

Second, the calculation is uniform and therefore good at analyzing and ranking various investments and/or projects equally.

Finally, because IRR is a discount rate that yields a zero NPV, it is a reliable indicator of the potential return on an investment.

Typically, IRR is analyzed in conjunction with NPV to identify the best investment or use of capital across a wide range of investment opportunities. If solely relying upon IRR, then the opportunity with the highest IRR would usually be selected.

Businesses use IRR to analyze whether an investment or project yields, or will yield, a benefit in excess of the costs.

Additionally, IRR is capable of analyzing a wide variety of investment types because it is agnostic to industry or any other external factors, thereby leveling each investment opportunity and representing the expected return of each potential project.

One limitation of IRR is that the formula is not able to identify projects or investment opportunities with a larger cumulative payout over time.

For example, a project with smaller cash flows and cumulative payout over a shorter period of time might have a higher IRR than a project with significantly larger cumulative cash flows.

For this reason, IRR is often used in conjunction with other metrics to analyze investments.

How Is IRR Calculated?

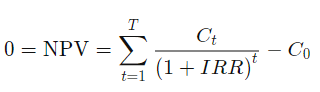

The mathematically approach to calculating IRR looks like this:

Where NPV is equal to zero and:

t = the number of time periods

Ct = net cash inflow during period t

C0 = total initial investment costs

IRR = the internal rate of return

Calculating IRR requires setting the NPV to zero and then solving for the discount rate needed to force it to zero. Because of this, the manual formula for calculating IRR is iterative and must be done through trial-and-error, making it difficult to do on paper.

In Excel, IRR requires a series of cash flows, with outflows being negative and inflows being positive with corresponding dates. The initial investment in the calculation must always be negative.

In certain circumstances, projects have both positive and negative cash flows during the same time period. In these cases the net cash flow can be used in the calculation and is sometimes referred to as the “net IRR”.

Calculating IRR in Excel

There are two ways to calculate IRR in excel, one is with the “IRR” function and the other is the “xIRR” function.

The primary difference between the two formulas is that the IRR function assumes equal time periods for all cash flows in a data series. Using the IRR function is appropriate if cash flows happen monthly, quarterly, or annually.

The xIRR function is appropriate when cash flows have irregular dates or if you know the exact dates of future cash flows. Typically, xIRR is considered to be more accurate than IRR.

Learn How Datarails Can Help Your Organization Create A More Agile FP&A Team

Datarails can help your company implement automation that can help your FP&A team operate more efficiently and effectively. Datarails is helping FP&A teams all over the globe reduce the time they spend on traditional reporting and planning, including IRR calculations.

By replacing spreadsheets with real-time data and integrating fragmented workbooks and data sources into one centralized location, you can work in the comfort of excel with the support of a much more sophisticated data management system behind you.

Build beautiful budgets, track and monitor business performance, and give users stunning and easy-to-use financial dashboards with Datarails.

Learn how Datarails has helped hundreds of finance teams streamline their operations.