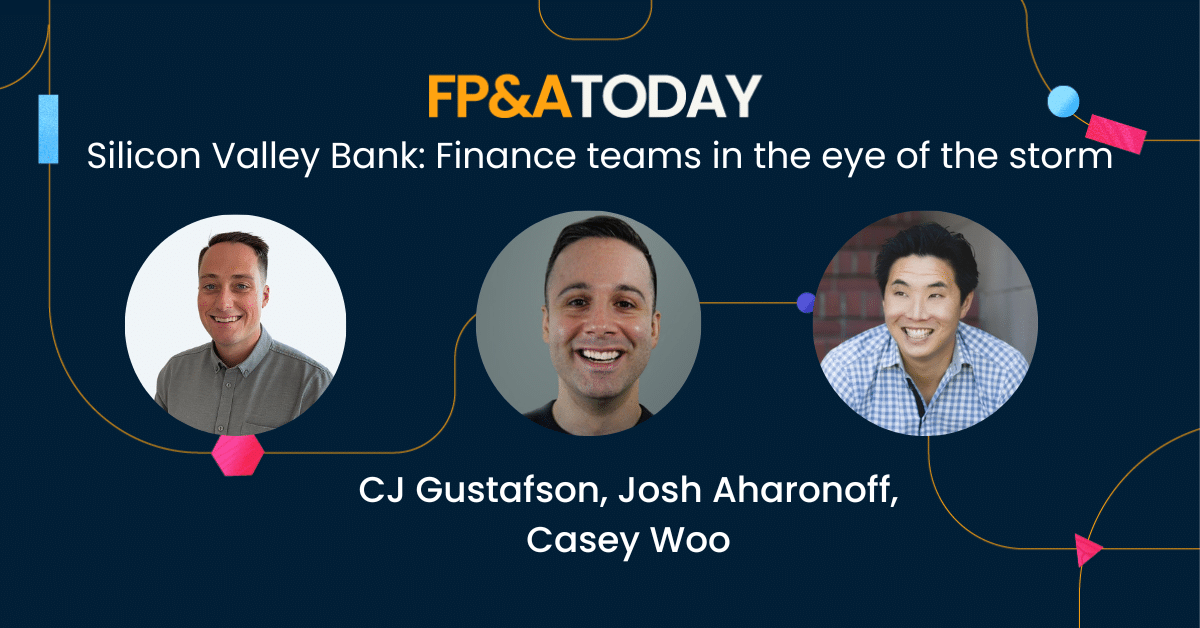

The second-biggest bank collapse in U.S. history created a storm for CFOs and their finance teams during a panic-induced 48 hours in March. It only ended as regulators took control of Santa Clara, Calif.-based SVB and a dramatic intervention by financial regulators.

In this special edition of FP&A Today, meet those in finance and FP&A who saw the events at Silicon Valley Bank first hand. Understand how the banking crisis played out and how ongoing ripples continue to impact everyone in FP&A and how your finance teams can cope with the ongoing aftermath.

The panel:

Josh Aharonoff (aka Your CFO Guy), CEO and Founder, Mighty Digits had many clients banking with SVB and had to make quick decisions as news broke. He shares Finance & Accounting Best Practices & Advice everyday to his nearly 85,000 LinkedIn followers

CJ Gustafson is a CFO at a series B startup, PartsTech. He has been in the startup space within the private equity sector and has helped to scale venture backed companies for the last 10 years. He also authors Mostly Metrics, an irreverent and analytical spin on metrics which has crossed more than 10k subscribers.

Follow CJ Gustafson on LinkedIn

Casey Woo is a seven-time high Tech CFO- turned investor. He has held finance and CFO roles at Silicon Valley companies including at WeWork and property tech companies before founding an “operators community” turned investment fund FOG ventures.

What is covered in this episode:

- Casey Woo explains being at the “heart of the storm” in Silicon Valley with a close personal relationship with SVB

- The reasons that VCs put pressure to withdraw money from SVB in a classic “prisoner’s dilemma”

- How the fallout from SVB continues to impact companies and particularly finance professionals

- The challenges for CFOs, particularly in tech, seeking to fundraise after SVB’s crash

- What are the differences between fractional banking and Ponzi schemes

- The initial $250,000 ceiling on federal deposit insurance explained

- How could KPMG have given SVB a clean bill of health with so many stored-up challenges?

- Why is the impact of raising rates so dramatically different than in the 1970s when no banks failed?

- Strategic advice for Treasury and FP&A pros going forward post-SVB

- The importance for CFOs and FP&A leaders to understand “second order effects” beyond cash entering and leaving the building.

- How the SVB saga has emphasized the value of an FP&A function that can show everything that’s happened, is happening, and is going to happen “and being in control of that story” – allowing you to take action quickly.

FP&A Today is brought to you by Datarails.

Datarails is the financial planning and analysis platform that automates data consolidation, reporting and planning, while enabling finance teams to continue using their own Excel spreadsheets and financial models.

Paul Barnhurst:

Hello, welcome to today’s FP&A Today podcast. I’m really excited to talk about what just happened over the last few days with Silicon Valley Bank. So we’d like to welcome all of you. If you can hear us there out on LinkedIn, just go ahead and put something in the comments. Let us know that you can hear us talking here. I’m going to start real quick by just covering a few items before I introduce our guests. So first, as mentioned, this podcast, we set this up over the weekend. We’re going to talk about what just happened with the banking situation and how that may impact people in FP&A. We have a couple CFOs with us and we’re hopefully going to have another guest here join us shortly. And then also, I just want to remind people, we also released today our podcast episode. You can go to any of your podcast sites to download that about chat, GPT by Glenn Hopper.

He built an FP&A tool. And then the other exciting thing is Chat GPT 4 was just released. So a lot going on at the moment. Thanks Mark for confirming the audio is good, Zach. Appreciate that guys. So what we’re going to do here is we’re going to go ahead and introduce our guests and then we will get into some of the questions we have. And please, we’re going to allow you as an audience to ask questions as we go throughout this. And hopefully we’ll have another panelist join us here shortly. So Josh, why don’t I start with you? If you could go ahead and take a minute and introduce yourself.

Josh Aharonoff:

Sure thing. Some of you may know me as my LinkedIn persona, Your CFO Guy. I am the CEO of an exciting company called Mighty Digits. We are a finance and accounting consulting firm for startups. And I post every day finance and accounting tips on LinkedIn.

Paul Barnhurst:

Thank you, Josh. We’ll next go to CJ if you just want give a introduction there.

CJ Gustafson:

Thank, thanks for having me on. So my name’s CJ Gustafson. I’m a CFO at a series B startup. I’ve been in the startup space on the private equity side and helping to scale venture backed companies for the last 10 years. So excited to be here.

Paul Barnhurst:

Great. And then Casey. Woo, if you could introduce yourself to the audience.

Casey Woo:

Hey everyone. Sorry I was lost in the Microsoft Teams link. Sorry My name’s Casey Woo, based in San Francisco Bay Area. I’m a recovering Wall Street investor, current startup operator. I would, I’d be what you call an operating CFO. So I have C,A, B, C, D, pre-IPO, most notably at WeWork. I have a lot of stories there. I think more importantly though, as my side project is called the Operators Guild, which has become more than a side project and it’s home to 700 of the world’s top operators in the world. CFO COO, BIS op strategy. Thanks for having me

Paul Barnhurst:

And thank you for joining us. So I chose these people cause I feel like each one of them would have a different perspective here. I’d invited a few others as well, but unfortunately some of ’em were caught up and busy with things. Obviously given all that’s gone on. So maybe we could just start with the question here and we’ll just start with you CJ, where were you when you first started hearing rumblings of what was going on over the weekend and what was your initial thinking before the government stepped in?

CJ Gustafson:

Yeah, I was actually at this very desk, but no, we started to hear rumblings from, actually I heard it from two sides. So I heard it from one company. I actually, angel invested in and his investors had reached out early in the morning on Thursday saying that they thought something was up with SVB. And then I heard from investors and kind of the community that I operate in as well. And at first I didn’t think it was a huge deal and then things just escalated really quickly. It was kind of like watching the Titanic go down in real time in the sense that it was just speeding up. And overall I was shocked that it kind of got to that point. It felt like, and this is just one guy’s opinion, it was a crappy hand that was dealt, but I don’t think it needed to go to the point that it went to. And I’m just happy at the end of the day that it sounds like when I was comparing this to a hurricane, you have different stages of it, whether it’s going to be a stage five, stage four, sounds like we’re getting out of this with maybe a tropical storm or a stage one, which is good to know that people have money in their operating accounts and can hopefully make payroll.

Paul Barnhurst:

Yeah, no, definitely some scary moments there. How about Josh, where were you when this first started happening and what was your kind of initial reaction?

Josh Aharonoff:

So I was actually in a meeting and I oftentimes get distracted, so I shut off all my notifications and when I came back on, I was about to hop to literally another meeting and I got a text from one of our clients saying quickly, this is really urgent, read the news with what’s happening with SVB, we have to transfer all of our funds. And I was kind of like, whoa, what are you talking about? And I Google and all of a sudden 40 different search results come up and I’m like, what’s happening? And then before you know what a ton of other clients start messaging me as well. So I got on a call with a few people from my team and I’m like, guys, what’s, what’s happening? What do we do here? And it was really just like, am I really experiencing this SVB? Everyone’s been banking with them. They’re like the number one in the startup space is this real? So it was just total shock.

Paul Barnhurst:

No, I could imagine. How about you Casey? I know you’re in the Bay Area, so you’re probably in the heart of all this. How did you hear about it?

Casey Woo:

We’re talking about hurricanes. There’s the heart of the storm and lemme tell you it wasn’t calm. And so I knew about this three weeks ago. So what happened was I knew there was something up. Yes, people joke, I should have bought, put options, but that’s a whole nother story. But so what happened was actually, and this has been lost in the whole thing, the credit goes to a Financial Times author. The article came out two weeks ago that SVB had problems. And what happened is in the og someone wrote hey, I know I see this article. What’s up with this? And of course other fact, SVB’s our longest standing sponsor at OG (Operator’s Guild). So I know them beyond well. So I’ll call him Bob. Bob is a 20 year veterans SVB calls me and goes, Hey, I hear an OG and stuff. They’re talking about we have a liquidity situation with our bonds.

Tell them it’s not the case. I said, all right.Give me your quote, I’ll do it. But what I did tell Bob was, Bob, you’re going to be the last person to know if there’s a real situation because an event you think your CEO as SVB’s going to be like, Hey by the way, hey Bob, we got you can’t say a thing. So the most interesting thing about SVB is there’ve been a lot of commentary about the worst communication you could possibly have as a bank. Okay, fair. And then there’s A, they are a public company B, they’re a bank. They were struggling with how do you actually warn and assure CFOs, which is my entire community news is going to come out, it’s all good. How are you going to say that as a public stock? And how are you going to say that without panicking everyone?

And then I’ll fast forward. Then it really hit a week later where they posted that they did have indeed a liquidity situation with the duration problem. So I was like, oh my god, it is real. Sure enough, my friend Bob was telling me nothing was happening. He wouldn’t know either. Here’s how I knew though. We used to sit with all the CFOs. What really happened? The CFOs were like, let’s not overreact here because we all know what’s going to happen if we overreact. It was a massive prisoner’s dilemma. Yeah, we were all sitting there in the chat, sorry I’m taking over here because this was like what happened? Where I sat is where we pulled all the money and in real time what happened was I would get a text, I get another text, my board member just told me, take all the money out right now.

So what’s really interesting, who is the real boss of all the money? The board. The board is the representative investors that own a company. So CFOs were in this very weird, if I pull it, it’s going to force everyone else to pull. And then our bosses all came down on us, which is why there’s a lot of the VCs did it now can you blame the VCs? Their entire fund or half their fund could be wiped out. I get it. So it’s a prisoner’s dilemma plus you know some information, which means everyone get out because the ratting is happening. And then five calls came. I added up the math that was $1.5 billion just in the five people that talked to me. He goes, what would you do? Well I think the VCs are all pulling, I think you know what you have to do. And unfortunately that’s what happened.

Paul Barnhurst:

Thanks for sharing in that. And unfortunately it makes sense. It does. This was a classic prisoner’s dilemma, but I think you made a really good point. The run wasn’t dictated so much by the CFOs as it was the VCs, you know, heard Peter th on Thursday saying Pull all your money. You heard founders fund some others all mentioning, look, we’re telling all our clients, pull it now. And we all know what happens once you have a run, it’s very hard to control. And by Friday morning the government had to step in because the balance sheet was upside down. I remember being on a podcast as we were getting the news and we were talking about it live. It had just come across the news in the middle of our podcast and was kind of surreal to me. Cause I remember thinking that morning, yeah, I hadn’t paid that close attention.

Oh they’re going to survive. Maybe I’ll buy some stock. And they hadn’t updated to the after hour stock price. Well I’m not paying at that rate. And so I didn’t buy and I was really glad I didn’t put any money in. This is last Friday I considered it. Yeah, now. Yeah, exactly. Hey, I’ll buy you the uk. Could you guys see Silicon Valley Bank UK was bought for a dollar a dollar, a dollar 20. Actually fx, sorry, a pound. You’re correct. A dollar 20. Thank you CJ. So I’m just going to let our audience, if you guys have questions, please feel free to put ’em in the chat. Good, love to have you put your thoughts there. So next question, and we’ll start here with you on this Josh. I mean how do you think this plays out? We know the government stepped in. Do you feel like we’re past most of this or do you have any thoughts on how this continues to impact companies and particularly finance professionals?

Josh Aharonoff:

It’s a great question. So first, everyone kind of caught their breath after they let out a sigh of relief whenever they found the government was going to step in. And for the short term, it really is great news. I mean when I told my wife the news on Friday that SVB went under, she literally thought that someone had died with the way that I looked with I told her because it really was frightening. And I mean we don’t even bank with SVB, these are just our clients. You could imagine people who actually have their money there, their ability to make payroll, their ability to even just survive and all that. So I think many people are not really focusing on the long term effect that this is going to have with the government stepping in. And I think this is definitely not going to help the economy. My hope is that it doesn’t spread to other banks in which you have ton more serious issues. But I imagine this is not going to be good for inflation. I imagine ultimately things are probably going to get worse with the economy before they get better. And I’m just hoping that things don’t really spiral out of control from here.

Paul Barnhurst:

And we definitely saw a little bit of that Monday as what did they hauled it? Almost 20 banks at one point or another from trading Credit Suisse just had to do, they admitted to a material misstatement. None of their board got their bonuses and they have to restate some of their financials. So I mean obviously that puts a little bit of nervousness in the market. We all saw what happened to first regional yesterday if you didn’t, yeah, you probably should have what they dropped 60% at one point, which is very similar to what Silicon did. But they’ve rebounded. They look like they’re more stable kind of balance sheet. But definitely I agree, Josh, they’re still repercussions to come from this. It’s not something like this can just happen and then you move on the next week and everything’s fine. So Casey, how about what’s kind of your thoughts now as we’ve seen the government step in and as we move forward?

Casey Woo:

I’m just going to say my opinion instead of what anything could happen. Sure,

Paul Barnhurst:

It’s all opinion. If we knew we’d be rich.

Casey Woo:

I think the news is we had a really good, we were prepped pretty well after 08 of how to deal with default. So number one, number two is this is a lot smaller than 08. These are the issue here is an issue is the maturity issue as compared to inflated mortgages that that’s a bubble that needs to pop. So there’s definitely this accounting issue that’s very real that’s going to stem through the system of all your books are inflated and the accounting rule changes that’s going to cause the downplay. I think the more interesting thing that I can contribute is not necessarily macro, but it’s the tech world. So we just had a big session in OG about the downstream effects and it’s pretty fascinating. So for those of you who don’t know, tech has obviously gone undergone a recession and a dry up in capital in the last year. It was like heyday 2021 and then it started slowing. If you are a tech company for the most part, most of your life is raising money. If you’re a Walmart, no big deal. You’re not raising money. So your entire life is built around fundraising, which is what CJ and I do for a living is we fundraise, we’re CFOs at early stage, not EBITDAs age. So just think about that. Tech companies have to fund fundraise. They burn money like a rocket ship.

It’s already been hard. Point number 19, I’ve lost it. When you fundraise, you’ve generally fundraise for 18 to 24 months. All right, if everyone’s following me here, you’re already 12 months in, so I’m almost everyone has six to 12 months left.

What happened when the equity markets dried up? You turn to VC debt. So everyone had SVB debt, they had Bridge Bank debt to extend runway and get through to a better stage to get equity. So the biggest ripple effect is VC debt also drying up. So whatever you thought was 12 plus 18 months of runway with debt is now back to 12. VCs are more spooked, not less spooked. There’s only two places to get money: customers and investors. Investors continue to be wary and the tech recession is weighing on current and prospective customers. It’s a very hard time for smaller companies selling to tech.

So what happens is this what people don’t realize right now all CFOs and OG are looking at their sales pipeline and cutting it in half. All of a sudden all that money is going to come in to save you and your forecast that’s gone. So you’re wrongly just went from 12 to 8. And here’s the other downward effect: your receivables. People mostly think when you have receivables, you receive them even on the other side. When you don’t have money, you know what you do? Hey, accounting department, step aside, I’m taking care of what that means. I’m not paying until LinkedIn turns off my LinkedIn. So now the entire spiral’s going to happen where AR becomes a prepayment plan for everyone and I’ll end with this. So that’s a big downstream effect. Another one’s, all the VCs, why they’re pissed and worried they have to fund all the next fundraisers. What happens when you can’t fundraise your inside investors give you the money. So my prediction is there’s going to be a massive amount of inside rounds that happen because they have to. So VCs with their powder are now like, crap, we need to save who we have cause other VCs aren’t coming to save. That’s the next six, 12 months is my bad. So anyways, I think that’s where the whole tech world is now set back and they were already on their heels. That is a massive downstream effect.

CJ Gustafson:

So I’m going to say something and maybe we can park this and revisit it later. But I see, and I hate to be the guy who’s pointing out the differences in terms, but there’s a big difference between a bailout and an insurance plan. And there are people around this table smarter than me, but my reading of this is that the funds are coming from an insurance plan that banks pay into, whereas a bailout is with taxpayer’s money. And so I just wanted to throw that out there because I feel like in the news that I’m reading, it’s the whole political conversation of this, are bailouts good or bad for the economy? And I think it’s neither here nor there. It’s actually an insurance policy that it was doing what it was supposed to do. And I’m I’m pro insurance as a CFO who wears both belt and suspenders to work.

But in terms of what’ll change, I think to piggyback on what Casey was saying, bridge loans are kind of gone. Those are vaporized. And I also think it was kind of sucked how VCs had depended on and kind of begged the Silicon Valley and the PAC West’s of the world to, hey, help me out, man, do me a solid. This company really just needs a bridge loan to get by. I’ll make you whole in the future. And then this happens after thousands of bridge loans. So I think some relationships are irreparably damaged. I think on paper equity actually looks better if I’m going to have to lock up all my cash in one bank. There’s a risk factor in that that’s not baked in. But then again, Casey was saying the multiples probably aren’t going to look as great for equity. So you get that downstream effect.

And then there are longer sales cycles if your customers were worried about where they were going to get their payroll. There aren’t a lot of CFOs who are signing long-term three year contracts for software. They’re a little bit shell shocked right now and just trying to get their bearings and just going on in the background of all this, we got to remember that two weeks before this happened, there were a ton of companies who were burning a lot of cash and trying to figure it out. How do we right this ship? We’re already in a situation where we’re burning more than we wanted to and then they get this scare that on top of that their cash may be gone. I think this impacts people’s mentality of how they look at their operating plan. And there are a lot of people who were about to have to make really hard decisions around their work plans and their workforces and operating plans that are probably now sitting back like relieved but also more cautious than they were two weeks ago.

Paul Barnhurst:

So there’s clearly a psychological impact as well. You make some good points. The market had already been closed up to a certain extent for a while there. Companies didn’t know if they were going to get their payroll. I mean, I know somebody who spent all weekend trying to decide if his company would survive or not running cash flow and he set me a note, he’s like, good news, I think we’ll survive. I’ll still have a job come Monday type of thing. And then the announcement came out Monday. But just the reality of the stress of it, right? Many. I know people are VCs, I’m sure you do too, Casey. Just people freaking out and trying to figure out how do we manage this?

[Datarails ad] You know what it is like 13 different spreadsheets emailed out to 23 different budget holders, multiple iterations, version control errors, back and forth updates you never really feel in control of the consolidation and collection process. Yep, I’ve been there. Stop. Breathe

Data rails is the financial planning and analysis platform for Excel users. Data rails takes data from all your company’s disparate sources. No organization is too complex, consolidating everything into one place, secured in the cloud now all your data finally talking to each other, everything is automated. Back into your report in Excel. Cash flow, FX conversion, intercompany transactions now automated and up to date, drill down and variance analysis in seconds. Don’t replace Excel, embrace Excel, turn your Excel into a lean mean fp n a machine. Find out more@www.data rails.com.

So one question we had from Zachary. He said, should we continue to allow banks to use deposits to fund VC debt? That’s been a question that a lot of people have been asking. Any thoughts on that?

Casey Woo:

Is the VC debt product a viable one? Is that the question?

Paul Barnhurst:

Question is, should banks be allowed to use deposits to fund VC Ddebt since it’s a higher higher risk debt? Should they be able to do that with deposits? Is that a loan they should be able to make?

CJ Gustafson:

There’s almost some hidden risk in there that what they’re repurposing it for.

Paul Barnhurst:

Yeah, that’s a question people are asking

CJ Gustafson:

That That’s an interesting one because it’s a different risk profile that they’re taking. I guess in that investment strategy. The thing, and I’m not the best person to directly answer that question, but the thing that I think has to change is that the dirty secret is that in order to get a venture debt facility or revolver, you have to put all your cash with that bank that hold this collateral. But I think we’re starting to see the flaws in that system. That it’s riskier than you think. And I think boards are going to start to ask how many banks you bank with and then what the main activities you do with each of those banks are. So who’s your treasury partner? Who’s your day-to-day banking partner for AR and AP and payroll? Who’s your FX trading partner and what’s your plan of action if any of these kind of go out the window? So mapping out kind of your treasury stack I’ll call it.

Casey Woo:

Another big downflow is, I mean in the operator world, we’re all rewriting to go, by the way, if you want to join in, OG is writing a collective Wikipedia on a new way of running. So Treasury 2.0, cash management 2.0 and all the lessons learned exactly what CJ said. So that’s another one where the one of the effects is way better treasury. I don’t agree that series A companies are going to high treasurers. I think I agree that there’s going to be a lot more. It’s not just the bank account that does payroll. Okay, that’s kind of what it was at Startup land. It is way more sophisticated at this point thanks to this. This’s a very interesting question. I wanted to pause. The first thing I was thinking about is you get paid on the risk. So in theory it balances.

Let’s just say these are not 1% loans. Where it is messed up in a agree with CJ is that there’s a lot of, it depends on times are good, there’s markups on equity. So the other thing is you give equity to the SVBs of the world. Also, the fundamental flaw was when times were bad, guess what happened? This is what started the S VB problem. We pulled all our money out of SVB to use it. Oh by the way, it wasn’t coming back. Remember the fundraising pool, there was no new deposits and that’s where the string was pulled. Deposits were out to be lent. Now there’s no more refreshing. And then they took a big bet on interest rates. So there is a fundamental flaw with the double usage triple incestuous thing. It wants to tell.So that’s a good call.

CJ Gustafson:

It’s like the Russian doll, that one’s inside or the other. But you don’t really know and you have that ta, that long tail exposure to something that’s riskier than what you think.

Casey Woo:

That’s blew my mind. I didn’t like whoa,

CJ Gustafson:

Inception, man. It’s inception.

Speaker 3:

Yeah. Anyways,

Speaker 4:

I actually

Speaker 3:

Have, I’ve heard that question. That’s a really interesting one.

Josh Aharonoff:

If I could chime in, I’d love to ask actually a related question. I was talking to my cousin over the weekend before all the news came out on Sunday and I was explaining what happened and he asked me such a great question that I didn’t really know how to answer. He said, well what’s the difference really between a bank and a Ponzi scheme? Now obviously there’s a huge difference. It’s not a scheme. Banks are legal, they’re heavily regulated and all that. But how would you explain to someone the fact that a bank takes your money, gives someone else, and as long as you don’t call your money by the time they get it back, everyone’s okay.

CJ Gustafson:

I would say it’s called fractional banking in the US economy has grown by leaps and bounds compared to other economies because of it. But it’s also the reason why I think our economy can spiral out of control potentially faster than others.

Casey Woo:

Ones. Well what you’re right, I think part one variable is called trust, but the other is called assets. If that’s a real question. There’s assets, if this is an auto loan, if it’s a house loan.,

There’s a car behind it

A ponzi scheme is, I used it to buy my own Ferrari and I’m not giving you any collateral for it. That’s called stealing. Lending versus stealing there we go, lending versus stealing. There we go. That’s my answer. I try to get,

Paul Barnhurst:

Yeah, no, that makes sense. And I get what you’re saying, Josh, in the sense of fractional that you’re using people’s money to continue to lend and you’re not keeping it all. But there’s a risk profile to that. It’s not like you’re right, stealing it with the Ponzi scheme and just using other people’s money to cover your mistakes, to hide the fact that you’re stealing off the top like a Bernie Madoff or someone like that. So I think that’s a good point. That’s the difference. But I can see where people sometimes could wonder. But fractional allows us, has allowed us to grow substantially. As you mentioned, CJ, if they couldn’t lend more than they take in, we wouldn’t have grown at near the rate we would have because there wouldn’t have been the investment dollars to fund all the things we’ve done.

CJ Gustafson:

I have a question I’ve been thinking through too, just for the group and this whole thing around the $250K limit, it just, I guess the first thing is do you think it feels weird that it’s the same limit for companies and also individuals? I guess I could have the same $250k insured limit as a multi-billion dollar company. And the second thing is in Casey, just in terms of you running companies day to day, how many companies have you worked at? Were like $250k was an actual limit that if you’re at any semblance of scale, I feel like you need that for payroll. It’s just unreasonable

Casey Woo:

To think, I sent you CJ, the chart, there was a chart of how many percentage of accounts that were under 250 by May. SVB was 3%.

Paul Barnhurst:

Yeah, I saw something like that. If saw that number

Casey Woo:

30 to 50% and why? Because SVB is full of people like me that just raised $80 million. So you’re right, 250 is like, it’s a good question. But no, the concentration risk also exacerbated SVB. Cause remember the whole story I told you this is, so someone said it best, the VC goes, your entire runway is in your bank, hung up. Pull it. Whereas Walmart, what I’m making it up, those companies, it’s like they’re not scary, but it’s not their entire livelihood. And so once you put a gun literally to a company’s head, let me tell you, all relationships are out the window and that’s what happened, right? These are guns to all little baby’s heads that are not profitable and the insurance is not there.

Paul Barnhurst:

And it’ll, it’s a good question. And people have been asking that should a different limit for individuals versus companies because the reality company can’t take it and put it in all different banks. Sometimes payroll could be that or a big vendor, you need that much in one account to pay it. So I mean really it’s a pretty arbitrary number, especially for businesses. And I think we’ll see a lot of debate around should it be higher, which means then the insurance has to go up for the banks and where are they going to fund paying more to the government insurance charging us more. Yes, it’s not a taxpayer bailout, but we as consumers pay for it, right? And I think it’s the right approach to take through the insurance than a bailout personally, but we’re going to pay for it one way or another. The banks are going to recoup their cost.

Casey Woo:

By the way, has it been adjusted for inflation or has it been 250 for like 80 years?

CJ Gustafson:

Good point.

Paul Barnhurst:

Personally not knowing the way the government works, but I’m not sure on that. If anyone knows, Casey.

Casey Woo:

I’m not young and I think it’s still 250 and I’m 40 years old, so I think it’s actually at least been around for 30 years.

Paul Barnhurst:

Yeah, it feels like that. I don’t ever remember it being anything else. And I’m

Speaker 3:

Point CJ the whole time. I’m like, I couldn’t even think about 250 because it was so like a pimple, but it just seemed like this irrelevant thing.

CJ Gustafson:

I mean if you’re running a 10 person business, I’m sure it’s like fine. And that makes sense.

Speaker 3:

Individuals.

CJ Gustafson:

Or individuals. It totally makes sense. But Josh, to your, maybe there should be a different tier for LLCs with under a certain amount of people

Josh Aharonoff:

Maybe.

Paul Barnhurst:

And maybe there’s some other kind of different way to raise insurance beyond the banks. If you want to have a higher insurance level, there’s a little bit of a fee you pay to protect those deposits. I don’t know. There’ll be a lot of questions asked,

Casey Woo:

Is there a general insurance for all banks? The umbrella insurance for all banks has nothing to do with $250,000. I wonder if that’s a thing. Maybe that’s called the government, I don’t know. But

CJ Gustafson:

You just become too big to fail and then I

Paul Barnhurst:

Think that’s called Uncle Sam. Yeah.

Casey Woo:

Okay. But maybe out of this comes a pot of money just for banks to save each other. No different than auto insurance. But

Paul Barnhurst:

Yeah, that’ll be interesting. So I’m going to go through a few questions we had from people. So we have one here that said HSBC announced a purchase of SVB and assured UK depositors, their savings are safe. And the person asked, and I’ll just get your thoughts on this and I’ll chime in. Maybe I’ll ask you Josh, you said, are those deposits really safe? Do you see any reason people should be concerned if they’ve assured the deposits are safe?

Josh Aharonoff:

I mean I don’t see why they would be too concerned. At the same time it’s an assurance director from the US government. But I mean when you have a bank like HSBC, I mean I would take it as safety, but I think the biggest thing for me out of all this is just stay vigilant and don’t take anything for granted.

Paul Barnhurst:

And I would agree with that. I mean I think you can. The UK brokered that if it was involved in that transaction heavily. They’ve also said that the money will be safe. So I think you should feel good about it, but you also want to make contingency plans if something goes wrong. I think that’s at least my thought on that one. Someone asked, can you confirm shareholder funds is completely wiped out? My understanding, and anyone else, any of you can correct me is the governments have been pretty clear. Look equity holders, sorry you invested, you lost money. That’s how capitalism works. We’re going to help the depositors here, but there is no bailout for executives or equity holders. Is that all your understanding? Okay, good. It looks like everybody’s aligned on that. That’s easy one. Yeah. Yeah, that’s what I figured. That’s a pretty easy one. So another question here, which I think is really interesting. So KPMG gave a clean bill of health just weeks ago. The balance sheet of SVB doesn’t really imply it’s at risk based getting a clean bill of health. What’s your thinking, CJ? You’re nodding a little bit. Yes,

CJ Gustafson:

There’s, there’s probably a core accounting point of view and then there’s probably a risk officer point of view and then there’s probably a security analyst point of view in all this. And the right answer is probably a combination of all of them. So KPMG probably was right by the books and academically . They are very smart at what they do. But I think that it’s hard to untangle and also we talked about it at the beginning of this, but the social aspect of how quickly these things snowball, that’s really hard to predict. But it is odd that there were a couple people in the Financial Times and a couple of substacks were kind of pointing out some weird stuff that was going on and raising some flags. So if they saw it, I don’t know, maybe some other people should have saw it too.

Paul Barnhurst:

Yeah, no it sounds like there are definitely people weeks ago raising it and I saw a really interesting article that just went through step by step what happened here and it’s fascinating to read. Yeah, another one that’s interesting, someone pointed out and the answer is yes here hasn’t the chief risk officer position at s SVP been banking for a bit? And my understanding is that position they left June of last year I think it was, and they just filled it in January. So it’s hard to say that played a role cause there would’ve been somebody under them managing risk. It’s not like just because you don’t have the chief risk officer, your risk department gets shut down. Any thoughts on that?

Casey Woo:

It’s not a thought, but there was literally a meme going around. I don’t know if this is fake or not. Joseph Gentilly is the

I know the one you’re talking about. Yeah,

He’s a chief administrative officer of SPB Securities and he was also the CFO of Lehman. So he has an epic resume, but I don’t know how much, I think that the default is SVB was negligent. Like it’s a management fault. I think that’s the default. I think that’s the most common belief. And then the second is there’s a flaw in the fundamental system of how their business was built. The belief that they went wrong is duration obviously. So I have a good friend who’s a treasurer at Citi or former treasurer and I asked him, I go, dude, what happened? He’s like, they did their job, they took their money and they put in treasuries. They didn’t go put in crypto, but they go, but it’s 10 year if my facts are right, they’re like 10 year. They’re like, yeah, they were long-term duration.

If I’m a treasurer senior, they’re eating my Cheerios oneof the things I would think about is what happens if interest rates go up? And I think what they said with the thought process at the time, you have to think about at the time it was, well, interest rates went up before whatever, we have enough deposits. So what I really understand of the SVB’s history is they had the most incredible deposit run you’ve ever seen. So I think it was lulled into complacency of we’re always going to have the deposits, everything will be fine. Right now if the funding environment for VCs continued deposits would’ve stayed high. So they just took a bet. And that’s the question is so translation, they should have hedged. They should just hedge the whole thing out. But they’re also a public company that’s looking for yield. So you have a pressure on management to grow the stock price, which is basically net interest income. So once you hedge out any benefit, whatever, but what they should, that’s the should of would’ve could have if it goes up. Okay past this point, that one hedging thing that did not happen because they took a bet on deposits and the good times to rolling. You tell me whose fault that was.

CJ Gustafson:

And there were kind of two cold ironies wrapped up in this whole thing. I wrote about it in my newsletter. It’s called – shamelss plug – mostly metrics. But the first one was that SVB became one of the country’s largest banks specifically by making a long-term concentrated bet on startups. But then that ended up being the demise for the same reason because the demographic of their customers was so highly correlated. And then the second thing, and this goes to what Casey was saying about the duration is that they bought these US bonds, which means they were actually giving cash to the government. But then where it went wrong is that the government was the one who raised the interest rates. And that was kind of a catalyst in it all. So I don’t know, there was just something that felt ironic about the fact that they gave cash to the government and were locked into these long-term US guaranteed treasuries and mortgage backed securities. But then the government cranked the rate up and that’s where they got caught in that what they call a maturity mismatch.

Paul Barnhurst:

As I’ve heard some people say, when you see rapid interest rates, right interest rate hikes, you often have on intended consequences. And nobody anticipated this happening. Now should a Silicon Valley bank hedged sure should. Have they saw some of the deposits at the end of the day? Was there some mismanagement? Yeah, we could all argue there was. I mean they’re gone. So obviously what, not saying intentional, but they should have managed it differently and they’d still be here. But you’re right, there is the fact that the government, which is really ironic that one of the things that did ’em in is putting their money in something that’s considered risk free, but it’s only risk free from the fact that you’ll get your money back out. It’s not risk free from an investment interest rate risk. And this really highlights that there’s more than one angle to risk free.

And I think a lot of times didn’t in the last few years, we haven’t had to think about that, right? Interest rates have been zero, near zero for so long that nobody’s thought about interest rate risk. So I think there’s also a sense of kind of lulled into security from the last decade a little bit, at least locally, internationally, a lot more interest rate risk. But when you’re dealing with the government, the rates have been pretty rock bottom for a long time now. And I can see Casey thinking there, I could tell you has something to say. Well,

Casey Woo:

Yeah. What’s interesting is the very commonly, and this is where you learn this by psychology for the masses, including myself, most of the time we think very linearly that that’s just a very common human thing. We don’t see weird, crazy black swans. And so what I’m saying is when you look back at crises, this is the KPMG audit question. Yes, the books look good. What they’re not paid to probably do is play out Montecarlo scenarios of correlation. So the correlation, so we build this system, as Josh was saying, it’s this interesting legal Ponzi scheme where we all rely on each other until it doesn’t. And so every day we wake up it’s like it’s working, so it should keep working, it’s working, but it’s very hard to fathom the correlation. It happened with God, what was the Russian Rubel crisis? Don’t, it’s just like 30 years ago where the hedge fund collapsed everything because it was also a system of it’s working until it’s not.

So if you think about that oh eight and here even covid a high correlation of different things,. What I’m starting to realize is there’s so many underlying correlated risks in our world that are just hidden beneath the surface. And just give me another one. I don’t know what it is, but that’s how humans build things is on trust and like greed, right? . That’s how Wall Street gets built. More products, more services. Something is building in some bubbles, building, you’ll make a lot of money if you find the next one.

Paul Barnhurst:

Agreed. So we have a question here from Veronica. She said back in the seventies, [Paul] Volcker [Chairman of the Federal Reserve] raised rates to fight inflation, but no banks failed. What’s different today? So I think the difference is the bank that failed here had a different profile from any bank in the seventies, a different concentration and also had deposits coming down because of that tech concentration and what was going on. So it’s kind of a perfect storm. It wasn’t just interest rates. If deposits had stayed strong, they would’ve been fine even with the interest rate rise because they wouldn’t have had to call a bunch of bonds and spook the market like they did and have the run. And so I think there is a combination of things there beyond just interest rates that caused that. Anything anyone would like to add to that question?

Josh Aharonoff:

Yeah, definitely. Initially I heard a lot of people talking about the fact, oh is all because the government raised interest rates, but you really hit that nail right on the head there that it wasn’t necessarily that the government raised the interest rates. It was that SVBs capital dried up and there were forced in order to fix their liquidity issues, to sell a bunch of their available securities at a huge loss at the worst possible time. So it makes me wonder if they had adequate capital, if startups for a number of months before this thingswere still booming like were, like you said, Casey, in 2021, would we have had this issue? Tons of what ifs.

Paul Barnhurst:

And someone mentioned I think Russian flu when you’re talking about the Russian thing there, we got a comment there and some others. But I want to kind of go to a question here that brings us kind of full circle and back home. What advice would each of you offer to kind of companies going forward? What’s maybe a lesson they can take away from this, especially for treasury, finance, FP&A professionals, maybe CJ, I know you’re a CFO. How are you thinking about this in your company to just be prepared if something like this happens?

CJ Gustafson:

I think strongly consider the terms of your venture debt deals. Make sure that you’re not just getting in bed with the right partner, but the right terms and parameters of it, including where you get to park your cash. It’s a pretty scary thing that a lot of CFOs on Thursday had to make the choice of, do I rip my cash out and be materially in breach of the contract that I have? Or do I keep it in? And then I think you also want to dig into who your payroll provider works with. This is another thing that kind of went under the surface, but a scary subplot was that major payroll providers got caught in kind of the week. So a bunch of startups, you didn’t even bank with SVB, they got all jammed up because they used a payroll provider who did same thing with payment gateways. So I think as CFOs we’re myopically focused on how cash enters and leaves the building. And as finance leaders, you also got to dig into the second order effects of what happens in between those steps of when it enters and leaves the building.

Paul Barnhurst:

That’s a great point. That was something we discussed quite a bit last Friday, is how does this impact payroll processing? Because I was on the cloud accounting podcast and they immediately brought that up and payroll and how does this impact the technical rails that are going on of moving money with SVB, which I think often isn’t something you think about, right? You just think about, can I get my money out? Yeah, not all. Those second order things that you mentioned. Josh, what’s your thoughts? Any advice you’d offer here or lessons learned if you’ve gone through this?

Josh Aharonoff:

My biggest thing is really to own and be in control of your data. And that’s having lazer focus and understanding on what exactly is happening with your business. And that doesn’t mean that you’re spending three hours a day putting together complex models, but ideally you have a really strong FP&A function where you could understand everything that’s happened with your business, everything that’s currently happening, and then everything that’s going to happen and being in control of that story, allowing you to take action really quickly. I mean, startups are some of the fastest moving companies on the planet. Just waiting like a day or two like we saw from this experience can be just total catastrophe. So my biggest advice would just be being in control of your data at all times.

Speaker 2:

Thanks, appreciate that. Josh, how about you Casey? What would you offer?

Casey Woo:

My biggest? So funny enough, I see problems in two worlds. One is systematic and one’s idiosyncratic. Ironically, my wife will tell you I’m too cavalier. I ironically am not too worried about systematic a) if it happens to everyone. There’s generally a bailout of some sort if it happens to everyone. For example, I wasn’t worried of payroll, I really wasn’t. I knew, are you kidding me? You think politicians are going to let people not get paid? No, I was not worried about that all. You know what I was worried about? If you’re sitting at an FDA company, it’s your company. Idiosyncratic, no one’s going to save you. Okay, that’s your, so what does that mean? And it’s very similar what Josh was saying. Having been a seven time startup CFO, I’ve increasingly become more aware of risk. I was naive before. I think so many of usespecially in Silicon Valley, we’re very big optimists.

So I think the biggest one is we don’t look at the downside that much. So very, basically what happens is in budgeting, when people budget, some people have really serious downside scenarios, but no one can do it, right? No one’s like, yeah, whatever. That’s not going to happen. It’s happening now and it’s scramble time. Everyone has an upside plan. Everyone has a base case plan. So the other one is what’s really bad is when things go wrong and that’s when you’re really screwed, screwed. So I think it’s, to Josh’s point, what can happen to us? Focus on a downside case a little bit more than one hour. Roll it out. What happens? What happens? Right now there’s all these correlated effects. And as a former stock trader, what happens is if you think something’s going down, it goes down way more than you think, right? Things go bad, they generally go worse than you think. So whatever the human FP&A person is saying is downside is probably like no, for startups, it could just be bankruptcy. Maybe that’s what it is. And so they don’t even need to talk about it. So it depends on your stage.

Paul Barnhurst:

The really good advice there, I think in the scenario planning to focus more on the downside and have a plan for it. And you’re right, in some companies that maybe bankruptcy, but for others obviously you want to try to avoid that as you can. So at least playing it out and saying, okay, is there a way we can prevent bankruptcy? If things go bad, what would that look like? How would we do that? I think scenario planning has become bigger and bigger. And also Carlo, it was a great way in some situations, instead of if you can’t really assign proper waitings and you want to get a different statistical, run it a bunch of times simulation, that’s another great way to go. And it may reveal that, oh, this is a lot more risky than we thought. It may help you come up with some plans you wouldn’t otherwise have.

I’ll go to our audience and just see are there any questions from the audience that anyone has? Give them a minute here and then we’ll give everybody a last word and we’ll wrap up. I did notice one person said they think the limit used to be a hundred K for FDI insurance. And then after 2008 it went up. But I’m not sure some, I’m sure somebody will research that and come up with an answer. I’m not seeing any questions come through. I’ll keep an eye on that, see if anything comes through. But maybe let’s give each of you to kind of, I’ll give your last thoughts on this. Any kind of parting words that you want to share with the audience here. And CJ, we’ll start with you.

CJ Gustafson:

Yeah, I think that at the end of the day, you want to put yourself in every position to be in control of your destiny and you want to increase your surface area for luck. The more technology I think we introduce, it’s great and you see a lot of cool new tools coming out. I think what changed the most after I saw this is what can I do to have information faster, to make better decisions across different systems? So it was a crazy situation that happened. I think we learned a lot from it. And you kind of control what you can control as someone kind of in tech that moves fast. And I appreciate the chance for, you know, invite me on too and to learn from you, Casey and Josh. So thanks.

Paul Barnhurst:

Yeah, thank you. CJ Casey,

Casey Woo:

This is, they sound like a shameless plug. It’s not. I get very often. So I’m a huge evangelist for startup operators. So everyone on this call, all the people who build every day, I love that. And that’s what I spend a lot of my free time doing so well. One thing I’ve always wanted to share, maybe I said in your podcast, Paul, is I get oftentimes for people who start in this business, is there a book? Is there an article? Is there a newsletter you could recommend me to? And I go into paralysis because I mean, can you answer that? I can’t answer that. But what I can answer, and there is an answer to this question. It’s community. When shit happens, think about your family. Think about when shit happens, which is what’s going to happen. You don’t know what the answer is. It’s called better together sounds cheesy, but Covid, PPP, SVB, the next one, the community I have, I won’t say the name cause that’s is saved me.

It’s saved a lot of us. And more importantly, it’s just like it’s lonely. So the loneliest time is when something becomes uncertain. You don’t really talk to your friends when things are cool. When things get weird, you all of a sudden talk to your friends and so you have friends. Why not have a professional community that’s always there for you whenever, and it’s incredible, the Wikipedia brain hive thing that happens when you have people dealing with a problem together and it’s bonded over it more. So whatever, what if you don’t have whatever community you have, what are friendships you have? Find one

Paul Barnhurst:

That is great advice. Having community, having mentors, having people that you can go to during difficult times, it can give you advice is invaluable, right? Because none of us have the answer to everything. We’re all learning every day and we should be learning from others. Yes. So Josh, what’s your, we’ll give you a final word here.

Josh Aharonoff:

I wish I went second because I’m just going to echo what Casey just said. But in the height of the panic, literally whenever the news went out that okay, they just went under. And I remember I was texting someone on LinkedIn because I don’t know, what does that mean at bank runs under, am I losing my money? And someone was telling, yeah, it could pennies on the dollar and we were hugely affected. We have tons of clients who are banking with svb and I’m going through these scenarios in my head, am I going to have to lay off half of my workforce? What’s this going to mean? And in the height of all that panic, I reminded myself what you mentioned, Casey, and that’s the fact that this is something that is affecting the entire tech scene. It’s not alone. Think about the scenario in which you get robbed and you get robbed and literally you’re completely alone and you’re freaking this out alone.

And this is a terrible thing. Everyone was going through this scenario together and it was still frightening. I still had no idea what was going to happen, but just the fact that all these people were interwined. On top of that, the fact that the government really is very sensitive with payroll issues, which would’ve been the biggest catastrophe. Mass layoffs, people unable to make payroll, that would’ve been the absolute worst and was said earlier, think of the PPP loan. Anytime there’s even the slightest confrontation between an employee and an employer, the government will almost always go on the employee side. No doubt that about it. So reminding myself of those things and having this amazing network of people who I could reach out to just to learn more about what exactly happened, I think was the most powerful thing that just kept my sanity and all of that.

Paul Barnhurst:

And thank you for sharing that, Josh. And I know you and I had a few messages back and forth and I know I had messages back and forth with friends that were going through all this, and it was good to get everybody’s perspective because it just helps ground you. It doesn’t necessarily make it easier, but it kind of puts grounding to it and reminds you that others are going through it and allows you to kind of push through. So I would just want to thank our guests. Thank you Josh, CJ, and Casey for being on, want to thank the audience, appreciate the questions today, and really appreciate you joining us. We’re going to go ahead and wrap up, but just a big thank you to everybody for joining us today.