Click for Quick Takeaways:

- Working capital performance is driven by timing metrics (DSO, DPO, DIO), which together determine the cash conversion cycle and liquidity.

- Delayed or fragmented AR, AP, and inventory data increases forecast variance and limits Finance’s ability to model cash flow impacts accurately.

- Manual, spreadsheet-based processes raise error risk and slow decision-making, especially during period close and forecast updates.

- Shorter cash conversion cycles directly improve liquidity, reducing reliance on external financing and emergency interventions.

- Real-time consolidation and scenario modeling enable Finance to quantify trade-offs, such as the cash impact of extended payment terms or inventory changes.

Picture this: Sales is on the verge of landing a whale by offering aggressive payment terms that will crush your Days Sales Outstanding (DSO) goal and strain cash flow. Now Finance has to step in and negotiate with internal partners to safeguard your precious liquidity. While Sales prioritizes growth and speed, you have to make sure the business is always in the black. Is there a way to improve working capital while giving your colleagues the flexibility they need to close the deal? Or will Finance be forced to act as the “Department of No”?

If it’s the latter, everyone loses. So why does this internal friction happen so often? Well, it usually starts when working capital, the lifeblood of the business, is managed reactively.

Improving working capital is clearly crucial for balancing stability with expansion, yet too many companies still rely on standalone spreadsheets and guesswork. And what they’re left with are unpredictable cash swings and unreliable forecasts.

Instead of fixing the core problems, CFOs and FP&A teams often attempt quick fixes for working capital issues. This might mean adjusting payment terms across the board, pushing suppliers or customers harder, or negotiating one-off contract tweaks.

These measures treat symptoms, not root causes.

The real culprits? Fragmented data and a resulting lack of financial agility.

Without a unified, real-time view of accounts receivable (AR), accounts payable (AP), and inventory, working capital will always be vulnerable.

The good news is that with the right approach, Finance can shift from being the growth “firewall” to the strategic enabler. Missed opportunities can be prevented with better working capital management.

With real‑time visibility and modeling tools, CFOs gain the confidence to say “Yes, if we simply adjust X or Y.”

This article explores how real-time consolidated data and automation empower CFOs to improve working capital without internal conflict.

It covers everything from core working capital components and why traditional methods fall short to modern strategies for unlocking liquidity and powering growth.

The Core Components of Working Capital Analysis

You’re no doubt familiar with the basic components of working capital: accounts receivable, accounts payable, inventory, and the timing interplay between them captured by the cash conversion cycle (CCC).

- Accounts receivable: Cash owed to the business from customer invoices. If invoicing is slow or collections drag out to 60+ days, your DSO (days sales outstanding) spikes, and cash gets stuck in receivables. In fact, about 70% of companies report a DSO of over 46 days, causing serious cash flow disruption.

- Inventory: Cash tied up in products or materials waiting to be sold. Excess stock or slow-moving products tie up money that could be used elsewhere, increasing DIO (days inventory outstanding).

- Accounts payable: Cash owed by the business to suppliers for goods and services. If procurement negotiates inconsistent supplier terms across departments, you might be paying some vendors too quickly, hurting DPO (days payables outstanding).

The cash conversion cycle metric combines DSO, DIO, and DPO to measure this timing. In simple terms, shorter cycles are better: a lower CCC means cash moves faster through the business, boosting liquidity.

Although most finance teams monitor these elements to some degree, common bottlenecks persist. The cumulative effect of these issues is a longer cash cycle and limited liquidity. Forecasting is also harder; each inefficiency adds uncertainty to your cash flow predictions.

With the help of working capital forecasting, however, you can build a bridge between day-to-day cash management and your broader financial forecasting and budgeting processes.

Done right, it projects how changes in AR, AP, and inventory will impact cash flow in future periods. This requires reliable, consolidated data and agile planning tools.

Financial forecasting and working capital planning go hand in hand: accurate forecasts depend on understanding working capital drivers, and proactive working capital management feeds into more reliable financial forecasts.

Why Traditional Working Capital Management Fails

Most finance teams know what to monitor, but legacy processes make it hard to manage these drivers effectively.

Here are five main reasons traditional working capital management often falls short:

- Relies too heavily on standard spreadsheets

- Inconsistent, delayed data without a single source of truth

- A greater risk of errors when variance checks are done manually

- A lack of real-time visibility into AP/AR

- Forecasting that can’t adapt to shocks

Overall, traditional working capital management fails because it’s too slow, too siloed, and too error-prone. Finance ends up acting as the bad cop out of necessity, since their data is unreliable.

To truly improve working capital, CFOs need to fix these core issues.

Let’s talk about how to do that.

Working Capital Improvement Strategies CFOs Rely On

Improving working capital demands targeted strategies that unlock cash tied up in operations to maintain and increase business momentum.

Here are four core areas where CFOs focus their working capital strategies, along with ways to increase cash flow and efficiency:

1. Accelerating Accounts Receivable (AR) for Faster Cash Conversion

When it comes to AR, the goal is pretty straightforward: get paid sooner without alienating customers.

CFOs and finance teams use several tactics to accelerate collections and shrink DSO:

- Faster invoicing

- Automated payment reminders

- Credit risk scoring and policies

- AR aging dashboards and analytics

- AI-powered AR predictions

2. Optimizing Accounts Payable (AP) without Hurting Relationships

On the AP front, the objective is to manage outflows smartly: you want to hold onto cash as long as possible, but without damaging supplier relationships or missing out on discounts.

Top-performing companies carefully balance Days Payable Outstanding (DPO) to optimize liquidity.

Here are strategies CFOs use to optimize AP:

- Strategically negotiating better terms

- Dynamic payment scheduling

- AP automation for accuracy and efficiency

- Closer collaboration with Procurement

Optimizing payables is about being deliberate with every dollar that leaves your accounts. The best CFOs treat outgoing payments as a portfolio to be managed, not just as bills to pay.

By maximizing DPO (without overstepping into late payment territory) and using tools to manage payment timing, you free up cash to reinvest or buffer the company.

AR improvements and smart AP management can seriously shorten your cash conversion cycle on both ends.

3. Streamlining Inventory Management

For physical product-based businesses, a substantial portion of working capital often consists of inventory. Any cash spent on raw materials or components effectively sits idle until the finished goods are sold. As such, efficient inventory management is crucial if you want to improve working capital.

Businesses must have enough stock to meet demand (and avoid lost sales), but not so much that they have inventory (AKA: cash!) collecting dust on the warehouse shelf.

To streamline inventory management, businesses can employ a number of strategies, including:

- Demand forecasting

- Supplier reliability and lead time analysis

- SKU rationalization

- Optimizing safety stock levels

When these strategies succeed, they translate directly into working capital efficiency.

With faster inventory turnover (higher inventory turns, lower DIO), it will take less cash to generate the same revenue. On top of boosting liquidity, this can also improve profitability by reducing storage costs and avoiding obsolescence.

4. Cash Flow Optimization and Forecasting

Rather than managing the components of AR, AP, and inventory individually, CFOs are increasingly taking a holistic approach to optimizing cash flow. This means forecasting cash needs, planning for both the short term and long term, and attempting to anticipate the impacts of a wide range of eventualities.

In this case, relevant strategies include:

- Short-term cash flow forecasting

- Long-term cash flow forecasting

- What-if scenario modeling

- Accounting for seasonality and macro shocks

Now let’s look at how technology, especially data consolidation and real-time reporting, ties all these strategies together, while preventing conflicts such as the demands of Sales versus the needs of Finance.

How Financial Consolidation Can Improve Working Capital

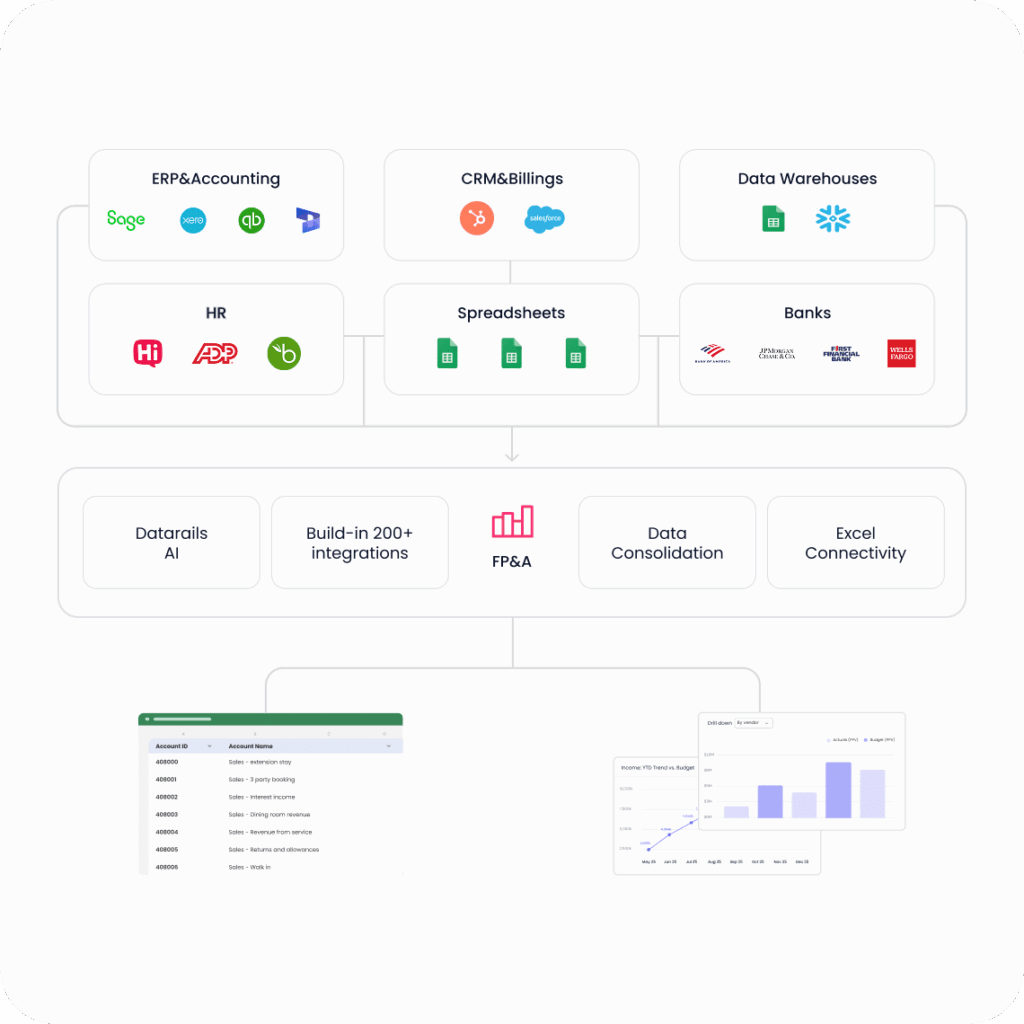

One of the biggest challenges in working capital management is key financial data being spread across many sources.

Payables, receivables, and inventory data often live in disconnected systems; you might have an ERP for payables, a CRM or billing system for receivables, a separate platform for inventory or supply chain, plus numerous isolated or shared Excel sheets.

This siloed setup makes it difficult to see the whole working capital picture.

As a result, actions to improve working capital are less effective because they’re based on partial information or outdated numbers.

Financial consolidation, the process of bringing all relevant data into one unified view, is a force multiplier for working capital optimization because it results in:

- Real-time, cross-organizational visibility

- Faster, error-free decisions

- Smoother communication via working capital dashboards and KPIs

- Reduced firefighting and more strategic planning

Datarails leads the industry in unifying data from all sources while preserving Excel workflows, giving finance teams instant insights without forcing them to use unfamiliar modeling tools.

With built-in analysis and scenario modeling, the platform turns Finance into a strategic partner that guides key business decisions.

Having covered strategies and general technological approaches, now we’ll look at how new technologies like AI and automation are further enhancing what finance teams can achieve.

Forecasting Working Capital with AI & Automation

Advanced analytics, artificial intelligence, and automation are reshaping the future of forecasting and managing working capital.

Here are some of the ways in which they’re already making a significant impact:

- Predictive modeling of cash flow drivers: AI identifies patterns in AR, AP, and inventory that traditional forecasts miss, improving accuracy and reducing surprises. It spots leading indicators early, helping teams prepare for shifts in demand or payment behavior.

- AI-driven AR collections: AI predicts late payments based on previous behavior and seasonality, recommending targeted collection actions to speed up cash inflows. It also flags anomalies so that Finance can intervene before overdue invoices turn into serious cash flow issues.

- Inventory optimization models: AI forecasts demand more accurately and adjusts safety stock in real time, reducing excess inventory without hurting service levels. This frees cash tied up in stock and improves liquidity.

- Automated variance analysis: AI pinpoints why actual cash differs from forecasts within seconds, saving analysts hours of manual work. These insights refine forecasts and help CFOs correct issues quickly.

- Real-time “what-if” adjustments: Scenario modeling tools let Finance instantly test the potential effects of updated payment terms, inventory changes, or sales shifts. The ability to pressure-test assumptions and hypotheses during high-level meetings strengthens decision-making and helps teams manage working capital with confidence.

- Better liquidity risk management: AI in FP&A predicts cash risks early, helping companies avoid emergency borrowing or last-minute interventions. Real-time visibility supports faster decisions and keeps liquidity stable even in uncertain periods.

The CFO of the future (actually, the here and now) can leverage these tools to ensure optimal liquidity and to guide their business partners with data-driven clarity.

How to Integrate Working Capital Optimization into FP&A Workflows

Implementing these improvements to working capital management isn’t a “one and done.” It will be an ongoing aspect of financial planning & analysis, so it’s one you want to be fully prepared for.

Here are some ways to integrate working capital optimization into your FP&A and broader business workflows:

Incorporate working capital in monthly/quarterly reviews:

Review working capital metrics alongside financial statements to maintain visibility into trends in DSO, DPO, and inventory turns.

Tie working capital assumptions to planning and budgeting:

Budgets and forecasts should include AR timing, inventory needs, and supplier terms. This way, growth plans reflect real cash demands.

In turn, this promotes healthy conversations about whether sales targets require more working capital and how to balance the needs of all stakeholders.

Aligning departments and breaking silos:

Finance should actively assist other teams in understanding how their decisions affect working capital, from sales terms to purchasing patterns. Regular cross-functional check-ins strengthen alignment on inventory targets, supplier terms, and customer policies.

Governance, policies, and audit trail:

Clear policies for payment terms, credit approvals, and inventory targets prevent one-off exceptions that weaken working capital.

Leverage technology as part of daily work:

Use existing systems for reconciliations, treasury alerts, and forecasting in order to spot cash issues faster and reduce manual work. Integrating data from CRM, procurement, and finance platforms gives FP&A a fuller and clearer view of upcoming cash needs.

Continuous improvement and training:

Review AR, AP, and inventory processes regularly to find new automation and efficiency opportunities. Encourage teams to suggest ideas and recognize improvements that strengthen working capital.

The Future of Working Capital Management

The future of working capital management is real-time, predictive, and collaborative. The days of static reports and siloed efforts are fading.

With the right tools, Finance can better fulfil its role as the operator of a well-oiled cash machine, ensuring every part of the business has exactly what it needs to succeed.

Companies that embrace these changes will be more resilient and more competitive. They’ll turn their working capital into an engine that powers innovation and expansion.

And finance professionals, armed with better data, will cement their role as strategic organizational leaders.

If you’re ready to discover how you can improve working capital with the market-leading Excel-native FP&A solution, your next step is clear.

FAQs

CFOs can improve working capital by fixing inefficiencies like slow invoicing, weak collection mechanisms, and excess inventory instead of mandating broad cost cuts. Automating billing, reminders, and payment workflows enhance liquidity without adding friction for Sales or Operations.

Real-time data shows exactly where cash is stuck, guiding targeted changes that support, rather than disrupt, day-to-day work.

The biggest gains tend to come from tightening processes around accounts receivable and managing accounts payable more strategically.

Faster invoicing, proactive collections, and small reductions in DSO release cash, while thoughtful use of longer payment terms and payment scheduling preserves it.

Inventory optimization adds another layer, turning slow-moving stock into cash and shortening the overall cash conversion cycle.

Real-time analytics provides an early warning system, flagging overdue invoices, bloated inventory, or unusual outflows before they become cash emergencies.

Dashboards and alerts help the team act within hours rather than wait for month-end reports. Scenario modeling tools then show how big orders, new terms, or cost changes will affect cash, allowing adjustments before liquidity gets tight.

Working capital solutions reduce liquidity risk by keeping more cash available to cover obligations and smoothing short-term swings. They also lower reliance on expensive short-term debt, which cuts interest costs and exposure when credit conditions tighten.

Automation and controls, meanwhile, shrink the risk of errors or fraud, while better ratios and cycle times signal financial discipline to lenders and investors.

The first source is internal: collect receivables faster, minimize excess inventory, and postpone non-essential spending to free up cash.

If that’s not enough, CFOs can negotiate temporary term changes with suppliers or customers, then consider external services like credit lines, invoice financing, or short-term loans.

However, equity injections should sit at the back of the line, used carefully and with clear communication, because they carry higher costs. Stretching payables can also jeopardize key relationships.

Some of the simplest strategies small businesses can implement include invoicing promptly, following up consistently, and using simple accounting tools to track who owes what.

Negotiating clear terms with both customers and suppliers, plus keeping a basic 13-week cash forecast, makes upcoming challenges visible before they become crises.

As they grow, owners need to watch DSO, inventory days, and current ratios so that growth does not outpace cash and force them into emergency financing.

Key metrics include DSO for collection speed, DPO for how long you hold on to cash before paying suppliers, and DIO for how long inventory sits.

Together they roll into the cash conversion cycle, which shows how many days cash is tied up from payment to suppliers to cash from customers.

Current and quick ratios, along with working capital turnover, round out the picture and help benchmark how efficiently the business turns working capital into revenue.