Click for Takeaways: Month-end Close Automation

- What month-end close automation does: Software replaces manual coordination across reconciliations, accrual collection, intercompany eliminations, and sign-off workflows with a single, structured, system-driven process.

- AI impact is measurable: Finance teams using generative AI have cut monthly close time by 7.5 days, while shifting meaningful time from back-office processing to higher-value analysis.

- Four stages of close maturity: Most mid-market teams are still in manual or partially automated territory. AI-enhanced close, where the system detects exceptions and generates commentary, is where the largest remaining gains sit.

- 14 platforms, one framework: This guide covers the full market from lean close tools to enterprise consolidation platforms, with a decision framework to match your ERP stack, entity count, reconciliation volume, and Excel dependency.

It’s day two of the month. Your team just started the close. Again.

The next ten days look the same from month to month: chasing department heads for accrual submissions, manually exporting GL data into spreadsheets, reconciling intercompany balances across three entities, and building the P&L pack from scratch. All the while, a Slack thread documents every discrepancy, version conflict, and missed deadline.

On day 9, the CFO asks for an updated close timeline, but you don’t have one. You have a spreadsheet. On day 11, you finally close.

Not only are you two days late, but three analysts are exhausted, and the management pack is already being revised because someone found a coding error in AR.

Why Does Your Close Take 10+ Days?

This problem isn’t because of your people but rather because of your process. The good news is, this is a problem finance teams can fix with month-end close automation.

What Is Month-End Close Automation?

Month-end close automation refers to the use of software to systematically replace manual steps in the month-end close process. Within a single, connected workflow (rather than copious emails and spreadsheets), this covers:

- Task orchestration

- Account reconciliation automation

- Intercompany eliminations

- Accrual collection

- Audit trail generation

- CFO reporting

An ERP like NetSuite or SAP records transactions. But for many teams, close orchestration (task tracking, dependencies, sign-offs) and reconciliation exception management typically require additional tooling or modules beyond core ERP.

On the other end of the spectrum, a standalone FP&A platform handles budgeting and forecasting downstream of the close.

Somewhere in the middle, you have close management software.

Some modern platforms (including Datarails) combine financial close management and FP&A in a single environment, so teams don’t have to transfer data between systems.

Core Capabilities of Month-End Close Automation Software(and Financial Close Automation Tools)

You won’t get the same features from software to software, but the strongest month-end close software covers these core capabilities:

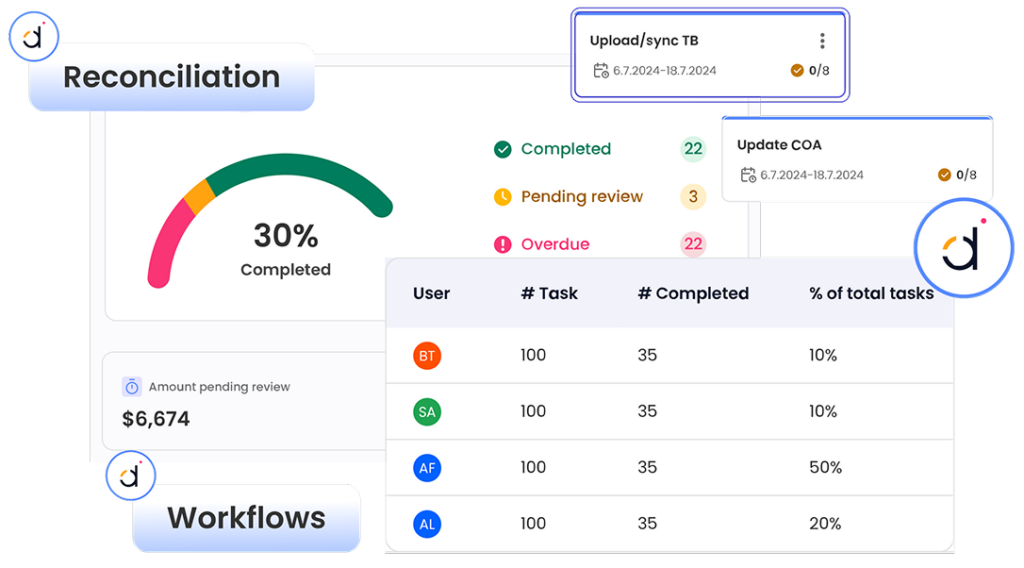

1. Automated Reconciliation Software

Rather than manually matching GL balances to bank feeds, sub-ledgers, or third-party statements, the system matches them automatically. This way, it surfaces only the exceptions that need human review and timestamps every step for audit purposes.

2. Close Task Orchestration

Previously mundane or time-consuming close tasks (including journal entry review, departmental accrual submission, intercompany confirmation) are automatically assigned, tracked, and escalated.

3. ERP and Data Integration

Real-time or near-real-time feeds from your ERP, bank, and sub-ledgers eliminate the manual export-and-paste cycle.

See more on data consolidation and how it speeds the close.

4. Multi-Entity and Intercompany Consolidation

With the help of automation, software can apply elimination rules consistently, flag out-of-balance intercompany positions, and produce consolidated statements without manual assembly.

5. Audit Trail and Compliance Controls

Software can automatically timestamp and log every transaction, reconciliation, sign-off, and adjustment. Internal audit, external audit, and SOX compliance are now a matter of running a report rather than reconstructing a paper trail.

6. Customizable Checklists and Workflows

A good month-end close checklist is only as useful as the system enforcing it.

Automated month-end close platforms let controllers build close workflows tailored to their entity structure, chart of accounts, and compliance requirements, rather than a generic template.

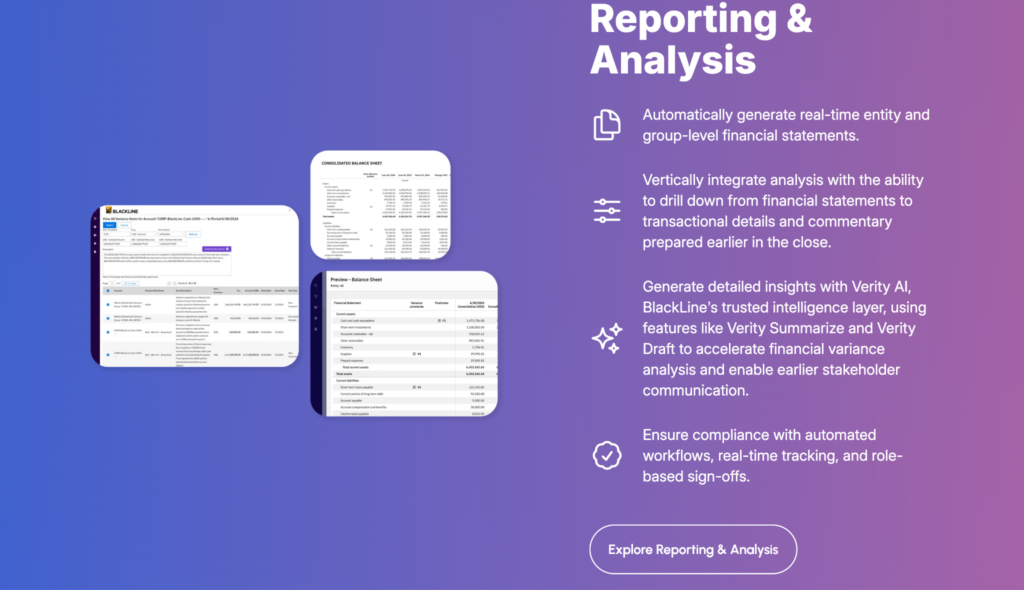

7. CFO Reporting and Financial Dashboards

Once the close is done, financial close automation platforms generate management packs, variance analysis and commentary, and board-ready reports directly from the close data.

See how financial dashboard software accelerates this last mile.

Key Use Cases for Month-End Close Automation Software

Next, take a quick look at at six use cases for financial reporting software to see some of the areas it brings the most value:

Reconciliation automation: For most finance teams, account reconciliation is the single biggest time sink in the close. Analysts manually export GL balances, pull bank feeds and sub-ledger reports, and match them line by line, every month. Automated reconciliation software eliminates that cycle by matching transactions automatically and surfacing only the exceptions that require human review. The result is that a process that previously consumed days of analyst time becomes a queue of flagged items, typically resolved in hours.

Close task orchestration: A close has dozens of interdependent tasks across multiple owners. Without a system managing dependencies, the bottlenecks are invisible until a deadline is missed. Close task orchestration assigns tasks automatically based on configurable workflows, tracks completion status in real time, and escalates items that are blocked or overdue. Controllers get a live view of where the close stands without having to chase updates across Slack threads and email chains.

Accrual management: Collecting accrual estimates from department heads is one of the most friction-heavy parts of the close. Requests go out, responses come back late or incomplete, and someone has to chase every submission manually. Automated accrual collection workflows send requests on schedule, track submission status, and route approvals without manual coordination. Coding errors caught at submission are cheaper to fix than coding errors found in the management pack.

Intercompany elimination: Multi-entity consolidation requires that intercompany balances reconcile before a consolidated P&L can close. Manually identifying out-of-balance positions across entities, resolving discrepancies, and applying elimination entries is time-consuming and error-prone. Close automation platforms apply elimination rules consistently each period, flag intercompany mismatches as they arise, and produce consolidated statements without manual assembly.

Audit readiness: An audit request that arrives after a manual close typically triggers a reconstruction exercise: pulling email threads, locating sign-off confirmations, and reassembling a paper trail that was never systematically documented. Automated close platforms timestamp and log every reconciliation, approval, adjustment, and sign-off by default. When audit season arrives, the trail is already there.

CFO reporting acceleration: The management pack is the last-mile deliverable of the close, and in most manual environments, it is also the most delayed. Data from the close has to be reformatted, narratives written from scratch, and the pack assembled and reviewed before it can be distributed. Close automation platforms generate variance commentary, management packs, and board-ready reports directly from close data, compressing the gap between close completion and reporting delivery.

How AI Is Changing the Month-End Close in 2026

A joint MIT and Stanford study published in 2025 found that accountants using generative AI cut 7.5 days off the monthly close, shifted 8.5% of their time from back-office processing to higher-value work, and improved the detail level of financial reports by 12%. For most mid-market finance teams, that gap between current performance and what AI-enabled workflows can deliver represents the single largest efficiency opportunity in the close process.

Month-end close automation is moving through four stages: manual, automated, AI-enhanced, and agentic. Many mid-market finance teams still find themselves in the manual stage. Best-in-class teams have reached automated. A growing number are now operating in AI-enhanced territory, where the system anticipates problems rather than just executing tasks.

The largest gains come from three AI capabilities:

Predictive exception management

Traditional reconciliation automation surfaces exceptions after the fact: the system runs the match, flags the discrepancies, and a human reviews them. AI-enhanced platforms go a step further by learning from historical close data to predict which accounts are likely to carry exceptions before the close even opens. Controllers can prioritize review queues based on risk rather than working through every exception with equal weight. Over time, the system’s predictions improve, and the volume of exceptions requiring human review decreases.

Automated narrative generation

Variance commentary is one of the most time-consuming deliverables in the close cycle. A finance analyst who can produce a management pack in three hours will still spend a material portion of that time writing explanations for variances they already understand. AI narrative generation reads the underlying data and produces first-draft commentary tied to actual movements in the numbers. The analyst reviews and edits rather than writing from a blank page. For teams producing commentary across multiple entities or business units, the time saving compounds significantly.

Agentic close workflows

The most advanced deployment pattern emerging in 2026 is the agentic close: AI that doesn’t just respond to inputs but initiates actions autonomously based on close status. In practice, this means workflows where the system detects that an accrual submission is overdue and sends a chaser without being told to, identifies an intercompany mismatch and routes it to the right owner, or flags an account balance that has moved outside its historical range and opens a review task before the controller notices. The human role shifts from coordination to exception handling and sign-off.

For a broader view of where AI is transforming finance operations beyond the close, see the guide to AI finance tools for modern teams and AI in FP&A.

How Many Hours Are You Wasting On Reconciliations?

“We cut the month-end close from weeks to just five days and saved 40+ hours a month.”

— Datarails customer

Top 14 Month-End Close Software and Platforms (2026)

The best month-end close software for your team depends on your ERP, entity count, reconciliation volume, and whether you need financial close management integrated with FP&A.

Below, we’ve detailed 14 of the leading platforms in 2026 to narrow down your search.

Automated Month-End Close Software Comparison (2026)

| Platform | Market focus | Core strength | Reconciliation depth | FP&A included | Implementation effort | Best fit |

| Datarails | Mid-market | Excel-native FP&A + close workflows | Strong | Yes | Moderate | Teams wanting automation without leaving Excel |

| FloQast | Mid-market | Close workflow + accounting operations | Moderate | No | Moderate | Accounting teams focused on close execution |

| BlackLine | Enterprise | High-volume close + matching automation | Very strong | No | High | Large enterprises with heavy reconciliation/matching volume |

| Workiva | Enterprise | SEC/regulatory reporting workflows (plus connected data) | Moderate | Limited | High | Public companies with significant compliance/reporting needs |

| Trintech Cadency | Enterprise | Financial close platform (incl. intercompany + reconciliation tooling) | Very strong | No | High | Enterprises with complex entities and close controls needs |

| Vena Solutions | Mid-market | Excel-based planning + financial close management | Moderate | Yes | Moderate | Excel-heavy teams wanting structured close + planning |

| OneStream | Enterprise | Consolidation + close in unified CPM platform | Strong | Yes | High | Large multi-entity orgs with complex consolidation requirements |

| Planful | Mid-market | Planning + consolidation/close capabilities in one platform | Moderate | Yes | Moderate | FP&A-led teams prioritizing integrated planning + close |

| HighRadius | Enterprise | Record-to-report automation (incl. reconciliation + close management) | Strong (esp. high-volume) | No | High | Enterprises focused on R2R automation and reconciliation scale |

| Numeric | SMB / lean teams | Lightweight close management + visibility | Basic–Moderate | No | Low | Small accounting teams needing fast close structure |

| Oracle FCCS | Enterprise | Consolidation + close in Oracle Cloud EPM | Strong | Limited | High | Oracle ecosystem orgs needing consolidation/close |

| SAP S/4HANA for Group Reporting | Enterprise | SAP-native consolidation + group reporting | Strong | Limited | High | SAP S/4HANA environments wanting native consolidation |

| Prophix | SMB–Mid-market | FP&A + financial close automation positioning | Basic–Moderate | Yes | Low–Moderate | Smaller teams moving off spreadsheets |

| Cube | Startups / scale-ups | Spreadsheet-native FP&A layer + monthly close reporting workflows | Basic–Moderate | Yes | Low | Early-stage teams wanting structured close reporting in spreadsheets |

1. Datarails

Recommended Mid-Market Excel-Native

Datarails is a month-end close automation and FP&A platform built for mid-market finance teams that want enterprise-grade automation without abandoning Excel.

The platform pulls live data from your ERP, automates reconciliations, orchestrates close tasks, and generates management packs, all from a connected workspace. Its AI layer adds predictive exception management and automated variance commentary.

Key features: Real-time ERP integration, automated reconciliation software, close task management, multi-entity consolidation, AI-assisted narrative generation, financial dashboards, and native budgeting and forecasting.

Best for: Controllers and FP&A leaders in companies with 50–2,500 employees who want close automation and planning in a single platform.

Pricing: Custom. Contact Datarails for a demo.

2. FloQast

Accounting-Focused Mid-Market

FloQast is a close management software built primarily for accounting teams. Its task management and reconciliation modules are impressive, and it integrates with most major ERPs.

The platform is less suited to teams that need FP&A capabilities in the same platform.

Key features: Request management, Excel integration, user-friendly dashboard, simplified SOX compliance.

Best for: Controllers who want purpose-built accounting close automation without broader FP&A requirements.

Pricing: Customized

3. BlackLine

Enterprise High-Volume Reconciliations

BlackLine is a leading enterprise platform for financial close automation. It handles high-volume reconciliations and complex multi-entity close workflows at scale. Implementation is substantial, and pricing reflects it.

The platform is best suited to large organizations with dedicated IT resources and a dedicated finance systems team, but it may prove to be too robust for smaller teams or those with more simplified needs.

Key features: Verity AI–powered automation, high-volume transaction matching, and end-to-end financial close capabilities.

Best for: Large enterprises processing thousands of reconciliations per period.

Pricing: Enterprise contract with customized quote

4. Workiva

Reporting-First Public Companies

Workiva is strongest in reporting (i.e., SEC filings, ESG disclosures, and related reporting workflows). Its close management capabilities are good but secondary to its reporting strength. Public companies with heavy compliance requirements are Workiva’s core market.

Key features: Data prep tool, traceable transformations for more transparency, live document collaboration.

Best for: Public companies with complex regulatory reporting requirements.

Pricing: Customized

5. Trintech Cadency

Enterprise Complex Eliminations

Cadency by Trintech is a mature financial close management platform with deep reconciliation and intercompany elimination capabilities. It’s designed for enterprise environments with complex entity structures and high volumes of reconciliation.

Like BlackLine, it requires considerable implementation investment.

Key features: High-volume account reconciliation automation, intercompany elimination, close task orchestration, risk-based reconciliation prioritization.

Best for: Particularly useful for enterprise finance teams in heavily regulated industries where SOX compliance controls are a priority.

Pricing: Customized

6. Vena Solutions

Excel-Native Mid-Market

Vena is an Excel-based planning and close platform that preserves spreadsheet workflows while adding structure and automation. Its close module covers task management and workflow automation; reconciliation automation is more limited than Datarails or BlackLine.

Key features: Vena CoPilot (agentic AI), workflow builder, centralized database, tax provisioning tools, audit compliance, version control.

Best for: Finance teams with a strong reliance on Excel and a preference for familiar interfaces.

Pricing: Customized

7. OneStream

Enterprise Consolidation-First

OneStream is a unified enterprise platform that handles consolidation, financial close management, and FP&A within a single, extensible data model.

Its close capabilities are suited to large, multi-entity organizations that need complex currency translation, intercompany elimination, and group consolidation alongside period-end workflows.

Key features: Multi-entity consolidation, intercompany elimination, close task management, currency translation, extensible solution marketplace.

Best for: Large enterprises with complex legal entity structures and high consolidation requirements.

Pricing: Enterprise contract with customized quote

8. Planful

FP&A-First Mid-Market

Planful is an FP&A-led platform with a dedicated Structured Close module that covers task management, accounting close automation, and close calendar management.

Its primary strengths are planning and reporting; close workflow capabilities are solid but not as deep as those of purpose-built close management software. Teams that prioritize integrated planning and close reporting in one system will find it a good fit.

Key features: Structured Close module, close task assignment and tracking, close calendar, integrated budgeting and forecasting, management reporting.

Best for: FP&A-led finance teams in the mid-market who want planning and close workflow managed from the same platform.

Pricing: Customized

9. HighRadius

AR/AP Specialist Enterprise

HighRadius is best known for its AI-powered accounts receivable and treasury management capabilities, but its Record-to-Report product extends into account reconciliation automation and close task management.

Its reconciliation engine is genuinely strong, particularly for high-volume AR and bank reconciliations. The platform is less suited to teams looking for a full-scope financial close automation solution that covers accruals, intercompany, and management reporting end-to-end.

Key features: AI-driven automated reconciliation software, bank and AR reconciliation, journal entry automation, close task tracking, and anomaly detection.

Best for: Enterprise finance teams with high AR/AP reconciliation volumes who want AI-native matching capabilities.

Pricing: Enterprise contract with customized quote

10. Numeric

Lean Teams Fast Deployment

Numeric is a modern, lightweight close management software built for lean accounting teams that want structured close workflows without the implementation overhead of enterprise platforms.

The platform covers close task management, reconciliation tracking, and review workflows, with a clean interface that accounting teams can get up and running in days rather than months.

Its reconciliation automation is less comprehensive than BlackLine or Datarails.

Key features: Close checklist orchestration, reconciliation workflows, review/sign-off workflows, dashboards, and Slack notifications.

Best for: Accounting teams of two to fifteen people who need close structure and visibility without enterprise-scale complexity or pricing.

Pricing: Its Essentials plan starts at $30/user/month. Growth and Enterprise plan pricing is customized.

11. Oracle Financial Consolidation and Close Cloud (FCCS)

Oracle Ecosystem Enterprise

Oracle FCCS is Oracle’s dedicated financial close management and consolidation cloud application.

Like most Oracle cloud products, it’s feature-rich but requires meaningful implementation effort and Oracle partner expertise to configure well.

Key features: Native Oracle ERP integration, multi-GAAP reporting, intercompany eliminations, close task management, consolidation and currency translation, and audit trail.

Best for: Mid-to-large enterprises already invested in the Oracle ecosystem.

Pricing: Quote-based subscription pricing

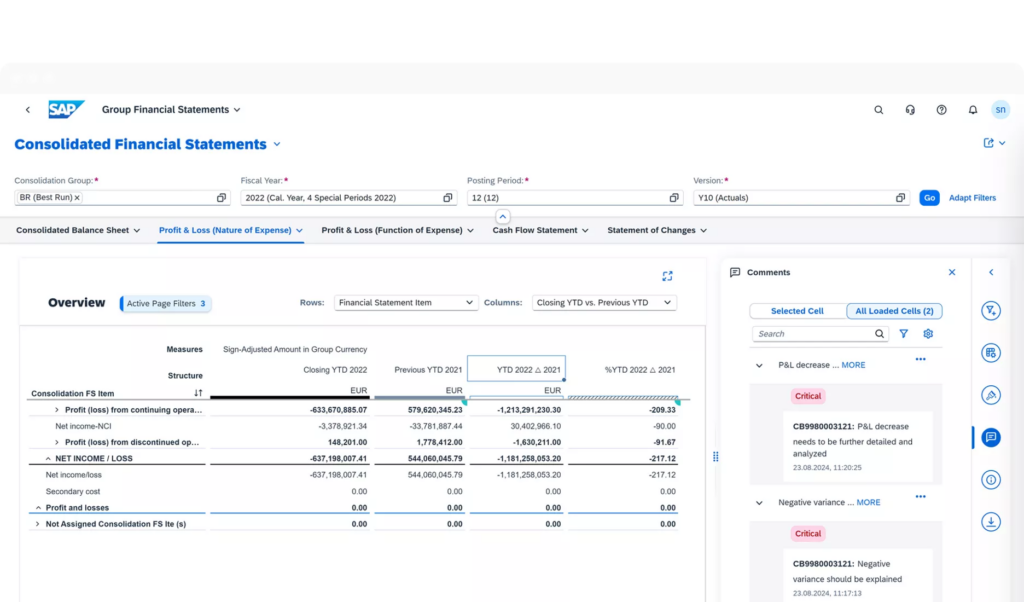

12. SAP Group Reporting

SAP Ecosystem Enterprise

SAP Group Reporting is the optional native consolidation and financial close management module within SAP S/4HANA. For organizations running S/4HANA, it provides real-time consolidation without a separate data pipeline.

Teams not on S/4HANA will find the integration case for SAP Group Reporting weaker.

Key features: Real-time consolidation from S/4HANA ledger, intercompany eliminations, currency translation, close workflow management, group reporting, and disclosure management.

Best for: Organizations running SAP S/4HANA that want native, real-time consolidation without deploying a third-party close platform.

Pricing: Pricing: SAP pricing is quote-based and depends on your S/4HANA edition, contract, and scope (often entity-/unit-based).

13. Prophix

SMB to Mid-Market Planning and Close

Prophix is a combined FP&A and close workflow platform for small and lower-mid-market finance teams. Its month-end close process automation capabilities cover task assignment, close calendars, and basic reconciliation tracking.

It doesn’t match the reconciliation depth of BlackLine or HighRadius, but for teams moving off spreadsheets for the first time, the platform provides an accessible close structure alongside budgeting and forecasting functionality without a large implementation investment.

Key features: Close task management, budgeting and planning, consolidation support, financial reporting, ERP connectors for common SMB and mid-market systems.

Best for: Smaller finance teams (typically five to twenty people) wanting close workflow structure and planning capability in one platform at a manageable price point.

Pricing: Customized

14. Cube

Spreadsheet-Native Startups and Scale-ups

Cube is an FP&A platform built around Google Sheets and Excel, offering a structured data layer without requiring teams to migrate away from spreadsheets.

Its close coverage is typically strongest on the FP&A side (data consolidation into spreadsheets, variance analysis, and reporting workflow) rather than acting as a dedicated, end-to-end close management and reconciliation automation system

Key features: Excel/Google Sheets sync, automated consolidation and variance analysis, reporting workflows, audit trails, and no-code integrations.”

Best for: Seed-to-Series B finance teams with lean headcount that want to add structure to spreadsheet workflows but may not need a dedicated close platform yet.

Pricing: Customized

How to Automate Your Month-End Close: A Step-by-Step Framework

Rather than a switch you flip, think of month-end close process automation as a migration from ad-hoc coordination to a structured, system-driven workflow.

Here’s a seven-step framework for getting there.

- Map your current close in detail

- Identify high-impact automation candidates

- Connect your data sources (data consolidation)

- Build your workflow in the platform

- Automate reconciliations progressively

- Establish digital sign-off protocols

- Track, measure, and improve

Need a more comprehensive starting point?

Get our free Month-End Close Checklist template. It was built for controllers who want a structured baseline before automating their close process.

How to Choose the Right Month-End Close Software

The best month-end close software is the one that matches your team’s specific constraints. Use this consideration framework to narrow the field.

Company Size and Close Complexity

Match the platform to your scale. Smaller teams benefit from lightweight tools, while larger or multi-entity teams need more structured or enterprise-grade systems.

ERP Stack

Choose a platform that integrates cleanly with your ERP. Does data sync in real time or rely on scheduled updates?

Reconciliation Volume

High transaction volumes require advanced automation and matching capabilities, while lower volumes can be handled within broader close tools.

Excel Dependency

If your team relies on Excel, prioritize platforms that support existing workflows instead of forcing a full system shift.

Compliance and Audit Requirements

Stronger controls, audit trails, and role separation become more important as regulatory and reporting requirements increase.

Time to Value and Total Cost

Look beyond upfront pricing. Consider implementation time, internal effort, and whether the platform delivers value quickly enough to justify the investment.

For lower volumes, the reconciliation module in a broader platform is typically sufficient.

Conclusion: The Cost of Staying Manual Is Getting Higher

A ten-day close is a liability. Every day the close runs past day five is a day the CFO is working from last month’s data, the board pack is late, and your finance team is buried in coordination overhead instead of analysis.

Month-end close automation changes the equation. Reconciliations run automatically, tasks assign themselves and escalate when blocked, data flows from the ERP in real time, and the CFO gets live close status from a dashboard, not a morning email.

Spreadsheet-based financial close management can’t answer the questions your organization is now asking. Month-end close automation can.

Datarails combines automated month-end close workflows with a full FP&A platform. Now, your team closes faster and plans better from the same connected workspace.

Explore financial close software from Datarails, or see how it fits alongside your existing budgeting and forecasting process.

Book a demo to see a live close workflow and get a close-time benchmark for your team.

Month-end Close Automation FAQs

Month-end close automation is the use of software to systematically replace manual steps in the financial close process.

This includes:

– Account reconciliation automation

– Task assignment and tracking

– Accrual collection

– Intercompany eliminations

– Sign-off workflows

– Management reporting

Month-end close software connects to your ERP and sub-ledgers to pull live financial data. Then, it automatically:

– Runs reconciliations

– Assigns tasks to the right owners based on configurable workflows

– Flags exceptions for human review

– Tracks close progress on a real-time dashboard

When the close is complete, it generates sign-off documentation and management reports directly from the close data.

Controllers typically report four core problems: close cycles that run ten days or longer, manual reconciliations that consume analyst time and introduce errors, no real-time visibility into close progress, and management packs that are completed too late to be useful.

An automated month-end close addresses all four directly: compressing close timelines, eliminating manual reconciliation, providing controllers with a live status dashboard, and accelerating reporting output.

The core features in a capable financial close automation platform are:

– Automated reconciliation software with exception management

– Close task orchestration with dependency tracking and escalation

– Real-time ERP integration

– Multi-entity and intercompany support

– Digital sign-off with complete audit trail

– Integrated reporting output

An ERP records and stores financial transactions, but it doesn’t manage close workflows, orchestrate reconciliations, flag intercompany mismatches, or provide a precise view of close progress across tasks and owners.

Close management software operates on top of the ERP, taking its data and applying structure, automation, and visibility to the close process that the ERP can’t provide natively.

Every reconciliation, journal entry review, accrual approval, and sign-off is automatically timestamped and logged within the platform. This creates a complete, searchable audit trail by default.