Click for Takeaways: Cash Flow Forecast

- Cash forecasting as a top priority: 73% of treasury practitioners now rank cash management and forecasting as their leading concern, yet 62% say it’s the most challenging task they face. A strong cash flow forecast template bridges that gap.

- Daily, monthly, yearly views: Cash flow projection templates serve different planning horizons: daily for near-term liquidity, monthly for operational cycles, and yearly for strategic runway. Each provides distinct insights that shape better decisions.

- Five-step template build: A structured approach based on beginning balances, flexible dates, input drivers, formulas, and validation turns a blank spreadsheet into a dynamic cash flow model template that minimizes guesswork and manual rework.

- Manual forecasting risks: Over 90% of spreadsheets contain errors, and 82% of small business failures trace back to poor cash flow management. Static models and fragmented data make these risks worse, not better.

- Automation and AI payoff: Connecting your cash flow forecasting template to live data and AI tools improves accuracy by up to 30%, reduces manual errors, and frees finance teams to focus on scenario analysis instead of data prep.

For many finance teams, cash flow forecasting still lives in spreadsheets built on assumptions that are outdated the moment they’re shared.

Revenue timing shifts. Customers pay late. Vendors renegotiate terms. FX rates move. Hiring plans change.

And suddenly, the “forecast” a CFO relies on no longer reflects reality. Yet despite this uncertainty, leadership expects finance to still be able to answer pressing questions such as:

- How long is our cash runway?

- What happens if revenue dips 10%?

- Can we afford to hire now?

- When will liquidity tighten?

These aren’t hypothetical concerns. The 2025 AFP Treasury Benchmarking Survey found that 73% of treasury practitioners now rank cash management and forecasting as their department’s top priority, up from 68% in 2022. At the same time, 62% say cash or liquidity forecasting is the single most challenging task they face. The urgency is real, but so is the difficulty.

Rather than a lack of data, the problem here is three-fold: fragmented data, static models, and manual updates. FP&A teams end up spending days reconciling numbers instead of analyzing outcomes.

By the time a forecast is ready, it’s already obsolete.

Modern cash flow forecasting requires the same mindset used in revenue forecasting: continuous, scenario-based modeling that’s directly connected to actuals.

Once financial data is centralized, updates are automated, and forecasting logic is layered on top of real cash movements, finance teams can move from backward-looking reports to forward-looking cash flow intelligence.

Instead of rebuilding models every month, teams can stress-test assumptions, simulate scenarios, and forecast liquidity in real time, all without leaving Excel.

Below, we’ll walk through how to build and use a modern cash flow forecast template. We’ll cover everything from setting up the structure to applying automation and scenario planning.

You’ll see how leading finance teams use templates not only to project liquidity, but to learn from real-time data, adjust faster, and answer the questions leadership asks most.

How Cash Flow Forecasting Templates Support Financial Learning

Let’s begin by discussing how cash flow forecasting can be a powerful learning tool for finance teams and business leaders.

Developing and using a template for cash flow forecast encourages teams to map out how money moves through the organization.

Cash flow forecasting templates support financial learning in numerous other ways, including:

- Strengthening understanding of cash timing and liquidity impact

- Variance analysis between forecasts and actuals, improving insight into inflows and outflows

- Refining assumptions and forecast accuracy over time

- Building financial awareness across departments and leadership

- Providing a clear, structured way to communicate cash priorities across the organization

Daily Cash Forecasting

Daily cash forecasting focuses on day-to-day liquidity. It’s especially useful for cash-intensive businesses or companies operating with limited cash buffers.

A daily cash forecast template lays out expected cash inflows and outflows, helping finance professionals ensure there’s enough cash to meet obligations at all times.

Monthly Cash Forecasting

Most organizations operate on monthly financial cycles, and monthly cash forecasting is therefore a core practice.

A monthly cash flow forecasting template projects cash flows for each month, usually over a 12-month (or longer) horizon.

Yearly Cash Forecasting

Here, the focus is on the big picture of cash over an annual or multi-year period.

Because the horizon is longer, a yearly cash flow projection template might be more high-level: you might not list every small expense category, but rather broad groups (e.g., total operating cash inflow, total investing cash outflow, etc.).

One common approach is to use a rolling forecast that extends 4 to 8 quarters out.

How to Build a Cash Flow Forecasting Template

Building a cash flow forecast template from scratch can seem daunting, but by breaking it into clear stages, you can create a reliable model for your organization.

Here are the key steps, with descriptions and examples, to guide you in constructing your own template:

Step #1: Start with A Beginning Balance

Make your starting cell the beginning cash balance for the period of time you are forecasting. The beginning balance will be used to calculate, or “roll,” the ending balance.

The basic formula is “beginning balance” + “Cash Received” – “Cash Paid” = “Ending” Balance.”

A simple way to begin building your cash flow forecast is to start with your beginning balance for the period and tie it to a bank statement or some other documentation.

Notice that the manual input is in blue.

Formatting is an important part of keeping track of which data fields are inputs and which are formula-driven.

Choose a color that will represent manual data input. In most scenarios, blue denotes manual data entry.

Step #2: Create Flexible Date Schema

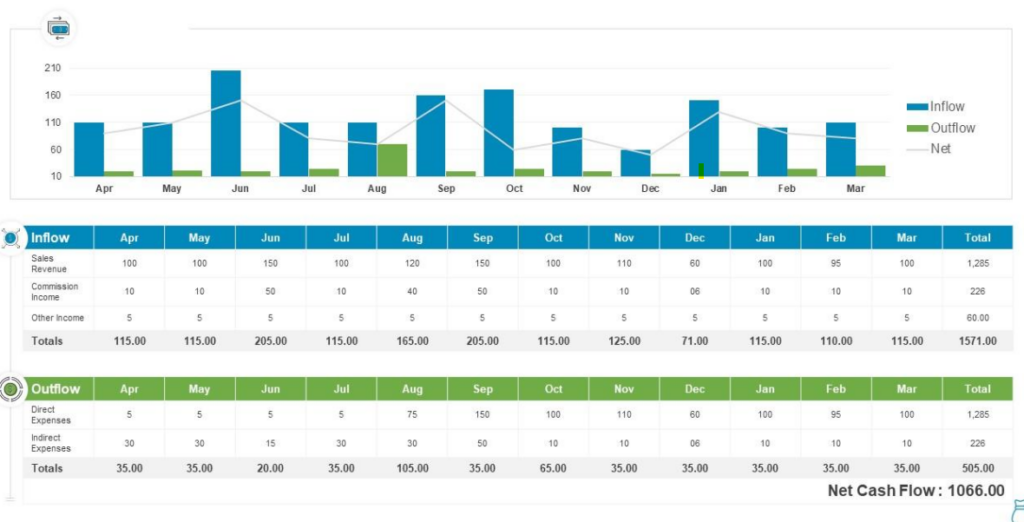

Aggregating data by month does two things: first, it creates a monthly cash flow forecast template, and second, it allows you to easily create a 12-month cash flow forecast template.

Creating columns for each month in the forecast results in a dynamic model that can be used in multiple ways.

This is an example of a date schema that will allow you to build a monthly, quarterly, bi-annual, and 12-month rolling cash flow forecast:t

Notice how the columns are grouped to present data by month, but are also consolidated enough to fit multiple months into one worksheet. This is an ideal cash flow forecast format for most businesses.

Step #3: Establish Data Inputs

Every good model should have isolated and static data points. One of the worst things for any financial model is stale data hidden within cells.

While there are many approaches to creating model layouts, one simple method is to allocate one column for each time period in the model to manual data inputs.

In a cash flow forecast template, identify all of the activities in the organization that drive cash receipts and payments. In most cases, fixed costs like salaries, payroll taxes and benefits, and rent expenses are easy to identify.

Remember, to exclude non-cash items on the income statement, like cost of goods sold, and replace them with cash activity related to acquiring inventory.

When establishing data fields, use names that perfectly match your budget. This will allow you to link the budget to your forecast to save time and make the model more dynamic.

The idea is to create a model that is flexible enough to use regularly, while also being a tool to measure the organization’s adherence to its fiscal budget.

Step #4: Build in Formulas and Links

Once you have your data structured and have a monthly template in place, it’s time to make sure all of your calculation fields make sense. In most cases, subtotals are used to aggregate cash flows into receipts and expenditures.

This makes rolling the beginning balance easier as you can simply add and subtract the appropriate subtotals.

Link your budget column to a dataset from a unified source. This is one limitation of Microsoft Excel: decentralized and separately managed workbooks for various types of information.

One way to bifurcate external links is to simply copy and paste the relevant data into a tab labeled “Data Input”.

When creating data tabs, clearly label them, and always ensure to maintain the integrity of the source data. Link the “budget” column in your cash flow forecast template to the relevant time period and data point in the source data.

This will allow you to copy and paste data from various time periods without having to update your column headings for a specific date.

Step 5: Validate and Iterate

With the template constructed, validate it against reality. If you have historical data, input a past period and see if the forecast would have accurately predicted the cash balance.

This back-testing helps ensure nothing important is missing.

Also, solicit feedback from others: treasury or accounting colleagues might spot issues or suggest enhancements.

Many finance teams eventually integrate their Excel templates with software solutions to pull in actuals automatically and push out updates.

For instance, using a system for data consolidation can feed actual cash numbers into your template without manual entry (ensuring you’re working with the latest data).

For a deeper exploration of advanced modeling techniques, check out our list of financial modeling tools and how they can complement your Excel-based templates.

Cash Flow Forecasting Formulas

At the heart of every cash flow forecast are a few fundamental formulas.

The most important one is:

Beginning Cash + Cash Received (AKA: cash inflows) – Cash Paid (AKA: cash outflows) = Ending Cash.

Others include:

- Net Cash Change: Net Cash = Total Cash Inflows – Total Cash Outflows

- DSO (Days Sales Outstanding): DSO = (Accounts Receivable ÷ Credit Sales) × Number of Days

- Projected Collections: Collections = Prior Period Sales × (1 ÷ DSO Adjustment)

- Payroll Calculation: Payroll = Headcount × Average Monthly Salary

- Interest Expense: Interest = Principal × Interest Rate × Time

- FX Conversion (for foreign currency cash flows): Converted Cash = Foreign Currency Amount × Forecast Exchange Rate

These formulas help structure your cash flow forecast template for clarity, accuracy, and scenario flexibility.

6 Common Challenges with Manual Cash Flow Forecasting

Basic spreadsheets are a familiar and flexible option, but manual cash flow forecasting involves various challenges:

- It’s time-consuming.

- The models are prone to errors (studies have found that over 90% of spreadsheets contain errors).

- Data is fragmented and not integrated.

- They’re complicated if you have multiple bank accounts and entities.

- Excel models are static by nature, even though market conditions aren’t.

- Scope for collaboration and scenario analysis is often limited.

For all these reasons, many organizations find that manual forecasting yields forecasts that are out-of-date as soon as they are produced. According to a U.S. Bank study, 82% of small business failures are tied to poor cash flow management, and the 2025 Cash Forecasting & Visibility Survey from Strategic Treasurer found that the share of organizations rating cash forecasting as “difficult” climbed from 39% in 2018 to 53% in 2025, while those calling it “easy” dropped from 28% to just 14%.

That’s why modern solutions and best practices directly address these issues.

How Automation Improves Cash Flow Forecasting Accuracy

Automation has been a game-changer for finance teams aiming to keep their cash forecasts accurate and up-to-date.

By automating parts of the cash forecasting process, companies address many of the challenges of manual forecasting head-on:

Real-Time Data Updates

One of the biggest boosts to accuracy comes from connecting your cash flow forecasting template to live data sources. Automation can pull in bank account balances, AP/AR ledgers, and other data around the clock, constantly updating your sheet. .

Automation can pull in bank account balances, AP/AR ledgers, and other data around the clock, constantly updating your sheet. Organizations that implement automated cash forecasting see up to a 30% improvement in forecast accuracy compared to spreadsheet-based methods, according to Gartner research.

Reduced Human Error

Automation significantly reduces the manual tinkering that often introduces errors.

If your forecasting process uses an integrated software or an FP&A tool, formulas and links are more likely to remain consistent, and the data is less likely to be mishandled.

Time Savings = More Analysis

Streamlining routine tasks (like data gathering, formula copying, and report generation) through automation frees up valuable time, which can be reinvested in analysis and scenario planning, improving the quality of forecasting.

Enhanced Scenario Modeling

Modern cash forecasting software often includes built-in scenario analysis tools. You can toggle scenarios (best case, worst case, etc.) with a single click, rather than maintaining separate sheets manually.

Better Collaboration and Version Control

Using an automated system or a centralized database means everyone works off the same single source of truth. When the data is consistent, the forecast’s accuracy improves.

Audit Trails and Assumption Tracking

Automation can log who changed what and when. This improves accuracy because you can work back through changes if something looks off.

Some advanced tools even require assumption inputs to be within realistic ranges or provide historical context.

Embracing automation, whether through specialized cash flow forecasting software or intelligent add-ons to Excel, is fast becoming a best practice in modern FP&A.

For a closer look at technology’s role in FP&A, read more about AI for financial modeling and how it’s changing the forecasting process.

Cash Flow Forecasting Scenarios for CFOs

CFOs use scenario planning to be prepared for whatever comes next. However, a single cash flow forecast isn’t enough.

Instead, you need multiple “what if” scenarios to understand the range of possible outcomes.

For example:

- Best-Case, Base-Case, and Worst-Case Scenarios: to help CFOs assess cash runway, plan contingencies, and use their cash flow forecast template to simulate different paths

- Revenue Downside Scenarios: to guide decisions around spending or hiring, especially in uncertain or recession-prone environments

- Delayed Collections (Receivables) Scenario: closely tied to working capital management. A PYMNTS Intelligence report found that 57% of invoices are paid late, with a third taking over 90 days to settle, making receivables timing one of the most critical variables in any cash flow forecast template

- Headcount Expansion or Reduction Scenarios: to help decide when to scale up or preserve cash in slower periods

- FX Impact Modeling: to measure exposure and inform hedging or reserve strategies, especially for international operations

- Fundraising or Financing Timing Scenarios: to show whether to adjust burn, line up credit, or take early action to avoid liquidity gaps

If you’ve built a solid cash flow forecasting template and ideally have some automation, you can adjust inputs to reflect each scenario and quickly generate new projections.

AI Tools for Cash Flow Forecasting

Artificial Intelligence is making major inroads in finance, and cash flow forecasting is an area seeing significant benefits from AI-powered tools.

Here are a few examples:

- Natural Language Processing (NLP) for Narratives: some platforms use NLP to explain changes in your cash flow forecast in plain language, helping CFOs quickly understand variances and communicate insights more clearly to stakeholders.

- Scenario Generation and Simulation: AI enables faster, deeper scenario analysis, like running thousands of simulations using Monte Carlo methods. It provides probabilistic outcomes and even suggests adjustments, helping CFOs optimize their cash flow forecasts.

- Automation and Anomaly Detection: AI can automatically reconcile forecast vs. actuals and flag unexpected changes. It also categorizes data, reducing manual work and helping teams respond faster to discrepancies in their cash flow forecast template.

AI tools are most powerful when combined with human oversight. They can crunch numbers and find patterns at superhuman speed, but finance teams still need to validate outputs and apply business judgment.

Incorporating AI doesn’t mean throwing away your existing cash flow forecast template.

In fact, many AI-driven solutions, like Datarails’ FP&A platform, work within Excel. They let you keep using spreadsheets as a front end while AI works in the background to pull data and run analyses.

You get the best of both worlds: the familiarity of your template and the power of AI.

For more insights on financial technology and automation, read about the top AI trends in finance and how AI finance tools are empowering teams to work smarter.

From Template to Action with Datarails

Once you’ve built a solid template and perhaps even integrated automation and AI, the next step is leveraging those tools to drive better decisions.

Datarails’ cash flow forecasting software ensures that finance teams are working with real-time data and integrates fragmented workbooks and data sources into one centralized location.

This allows users to work in the comfort of Microsoft Excel with the support of a much more sophisticated data management system.

Every finance department knows how tedious building a cash forecast template can be. Integrating cash flow forecasts with real-time data and up-to-date budgets is a powerful tool that makes forecasting cash easier, more efficient, and shifts the focus to cash analytics.

Regardless of the budgeting approach your organization adopts, it requires quality data consolidation to ensure accuracy, timely execution, and monitoring.

With Datarails’ financial planning solution, budgeting processes, profit and loss statements, and balance sheet statements are automated and simplified, as is scenario planning.

Ready to upgrade your cash forecasting process? Take Datarails Cash Management for a test drive to see the power of real-time, accurate cash intelligence for yourself.

Cash Flow Forecast FAQs

Cash flow forecasting is meant to ensure a business can meet its financial obligations and plan ahead.

It helps predict cash surpluses or shortfalls over time, so businesses can make informed decisions, avoid liquidity issues, and prepare for growth or downturns.

It should tell a business how much cash is expected to come in and go out over time, along with the projected balance at each point.

It breaks down expected inflows (like customer payments or loans) and outflows (such as payroll, rent, or loan repayments) by week or month. This helps businesses see if cash is building or burning, spot upcoming shortfalls or surpluses, and plan accordingly.

Cash flow forecasts also highlight timing issues, like seasonal dips or spikes, giving stakeholders a clear view of future liquidity.

Start with your opening cash balance and use a template or spreadsheet to project inflows (like customer payments or loans) and outflows (such as payroll, rent, and supplier payments) over time.

Next, apply the formula: Beginning Cash + Inflows – Outflows = Ending Cash, rolling the balance forward each period.

Base your estimates on realistic assumptions and update regularly with actuals. You can do this in Excel or with automated tools linked to your systems.

Automation improves cash flow forecasting accuracy in several ways:

– Timely data

– Fewer manual errors

– Enforces a consistent process

– More frequent updates

– Better integration with various data sources

– Better scenario handling

– More intelligent alerts and validations

The most common mistakes in cash flow forecasting include:

– Making overly optimistic assumptions about inflows

– Mixing up profit and cash

– Relying on static numbers instead of formulas or links

– Inadequate scenario planning

– Not reconciling the forecast with actual results periodically

– Not considering external factors (like interest rate changes)